McGlinchey: Trump's Damage To US Diplomacy Could Last A Generation

By Brian McGlinchey via Stark Realities

As the US-Israel war on Iran grinds into its sixth month, it’s clear to all but the most intellectually-dishonest Trump loyalists and war-bent Israel-sympathizers that it’s been a spectacular failure.

A war of aggression that was supposed to precipitate a revolution has instead galvanized popular support of the Iranian government in defiance of the country’s tormentors, who’ve killed thousands of their fellow citizens and destroyed civilian infrastructure. A war that was launched to neutralize Israel’s principal rival seems certain to leave that rival far more geopolitically powerful than before, while driving Americans’ support for Israel to record lows.

Beyond unforgivably throwing away the lives of 18 American service members in an unconstitutional war launched on false pretenses, Trump’s blunder has depleted America’s arsenal and pushed the country more than $100 billion deeper into debt. Meanwhile, the longer Trump delays the inevitable consummation of his defeat, the greater the risk of an economic calamity that engulfs not only the United States but the entire world.

If that latter nightmare can be sidestepped, we’ll likely find that Trump has inflicted his most enduring damage on an intangible yet critical national asset: the ability of American diplomats to productively engage counterparts all over the world. From using negotiations as a ploy for surprise attacks to murdering heads of state and casually reneging on American commitments — including his own — Trump’s damage to US diplomacy will be evident for years. Of course, that’s not to suggest America’s foreign policy reputation was sparkling before Trump’s ascension to power — only that he and his team have managed to drag it down to new depths.

Trump’s collaboration with Israel to launch an unprovoked war on Iran is manifestly among the worst foreign policy decisions in the history of the American republic. However, it’s important to appreciate that Trump first set this 2026 disaster in motion eight years ago: In May 2018, — spurred on by then-National Security Advisor John Bolton and Trump’s Israel-first donors — Trump withdrew the United States from the Joint Comprehensive Plan Of Action, or JCPOA.

Also called the “Iran nuclear deal,” the July 2015 JCPOA was the culmination of nearly two years of painstaking negotiations over highly technical provisions, conducted by representatives of not only the United States and Iran but also China, France, Germany, Russia, the United Kingdom and the European Union.

Under the JCPOA, Iran agreed to major restrictions on its nuclear program in exchange for relief from brutal economic sanctions. Among other things, the JCPOA required Iran to eliminate its medium-enriched uranium, slash its cache of low-enriched uranium by 98%, limit future enrichment to 3.67%, agree to even more external monitoring than it was already submitting to, and render its heavy-water reactor worthless by filling it with concrete.

Trump presents a memorandum reimposing sanctions on Iran after he withdrew from the nuclear deal at John Bolton's urging (Evan Vucci/AP)

Trump presents a memorandum reimposing sanctions on Iran after he withdrew from the nuclear deal at John Bolton's urging (Evan Vucci/AP)

Catering both to devoted Israel supporters and to Republicans who were eager to assume that a deal negotiated during the Obama administration must have been treasonous, Trump had repeatedly railed against the JCPOA throughout his 2016 campaign, declaring that his “number one priority is to dismantle the disastrous deal with Iran.” After being named national security advisor in April 2018, Bolton — who had long been pushing for war on Iran — quickly prodded Trump into making good on his promises to tear up the JCPOA, despite the fact that Iran was fully complying with the agreement.

“Trump’s move demonstrates that the United States cannot be trusted to keep its promises,” the Belfer Center’s Martin Malin said at the time. “It will heighten tensions in an already smoldering Middle East while giving fodder to hardliners and nuclear bomb advocates in Iran.”

After Trump’s withdrawal and the reinstatement of waived sanctions, Iran waited a year, but then began straying from its own commitments -- using elevated uranium enrichment as a lever to push for a new agreement and relief from suffocating sanctions.

Having long denied it was developing a nuclear weapon -- a claim repeatedly deemed truthful by the US intelligence community -- Iran returned to the negotiating table during Trump’s second term, once again ready to part with the uranium it had enriched to higher levels. Indeed, less than 48 hours before the United States and Israel attacked on Feb. 28, Iran offered concessions that included dilution of its 60%-enriched uranium, a multi-year pause on new enrichment, subsequent enrichment capped at 20%, and expanded IAEA oversight. UK national security advisor Jonathan Powell was reportedly surprised by the strength of the Iranian offer, seeing it as reason to hope war would be averted. His and others’ hopes were about to be dashed.

There are many facets of the Trump administration’s assault on diplomacy, but none more vulgar than using ongoing negotiations as a means of unleashing a surprise attack on a negotiating partner — an attack that includes the killing of that partner’s head of state.

That’s exactly what the Trump administration did to Iran in February. Having held a third round of talks in Geneva on Feb. 26, the two countries were set for what was described as technical-level discussions the following week. Instead, teaming up with Israeli Prime Minister Benjamin Netanyahu, Trump launched a massive war on Iran. In addition to killing more than 100 elementary-age schoolgirls and many other civilians and military conscripts, the opening attack killed Supreme Leader Ali Khamenei, his daughter, son-in-law and 14-month-old granddaughter.

Rubio further diminished US credibility by attempting to characterize the surprise attack as somehow defensive. “We knew there was going to be Israeli action” which would “precipitate an attack against American forces, and we knew if we didn’t preemptively go after them before they launched those attacks, we would suffer higher casualties,” Rubio said. Observers were quick to note that, regardless of Israel’s status as a sovereign state, its dependency on Washington means Trump held de facto veto power over an Israeli strike, which makes the rest of Rubio’s rationale hollow.

February wasn’t the first time that insincere Trump administration diplomacy set up Iran for a surprise attack. In June 2025, the administration had completed five rounds of negotiations with Iran and scheduled a sixth for June 15. On June 13, Israel attacked Iran. It was no surprise to Trump, who boasted that Israel informed him in advance. On June 22, Trump joined the 12-Day war via Operation Midnight Hammer, bombing Iranian nuclear facilities.

Beyond their fundamental immorality, these surprise attacks amid negotiations undermine long-term US interests by fostering distrust in everyone who witnessed such blatant American treachery. Following the start of all-out war on Feb 28, Washburn University law professor Ali Khan wrote about the consequences of turning negotiations into a “calculated ruse”:

“The breach of good faith signals worldwide that it is pointless to make any deal with someone who would do the opposite after creating an expectation or reliance for the other party. Iran or any other state would be highly reluctant to trust the Trump administration again in future negotiations.”

Note, one shouldn’t assume the world’s distrust will be so tightly associated with Trump that it will vanish when he leaves office. In Marco Rubio and JD Vance, his administration holds at least two potential successors to the Oval Office, to say nothing of senators, representatives and governors who’ve cheered on Trump’s misconduct and would be prone to emulating it. And don’t think for a moment that Democrats are immune to following unhealthy presidential precedents, whatever their commentary may be when those precedents are set by a Republican.

With his 2018 withdrawal from the JCPOA, Trump reneged on a deal made by another president, but Trump has repeatedly reneged on his own commitments too.

That’s the case with the June 17, 2026 Memorandum of Understanding between the United States and Iran, which Trump signed at the Palace of Versailles. Primarily brokered by Pakistan with help from several Middle Eastern states, the MOU has been described as an agreement to make an agreement. It comprises 14 points setting conditions for an immediate ceasefire and 60 days of negotiations for a lasting peace.

Trump quickly fell short of full compliance. “When you look at what’s happening from the Iranian point of view…the Iranians believe that the United States has not lived up to its part of the bargain,” University of Chicago international relations scholar John Mearsheimer said in July.

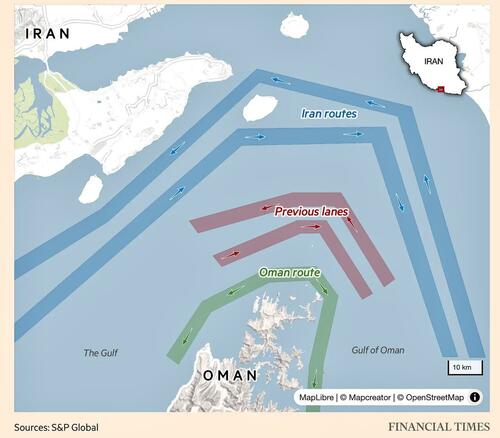

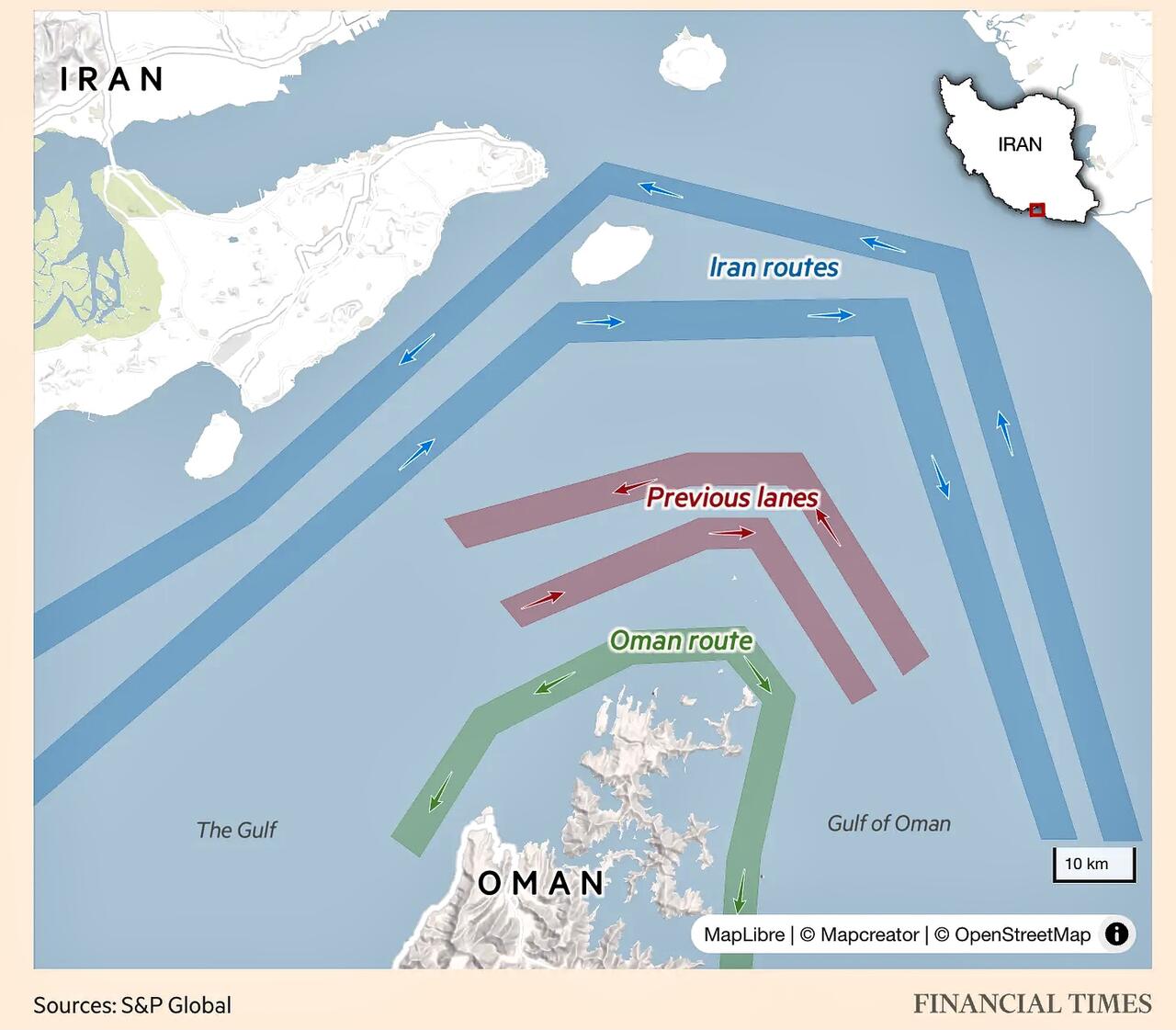

There are several elements where Iran reasonably accused Trump of noncompliance, but we’ll examine three, starting with the most significant one of all. Point 5 covers what has replaced uranium as the core focus of the conflict — Iran’s selective blocking of traffic through the economically vital Strait of Hormuz:

5: “Upon the signing of this MOU, the Islamic Republic of Iran will make arrangements using its best efforts for the safe passage of commercial vessels with no charge, for 60 days only, from the Persian Gulf to the Sea of Oman and vice versa.….[and] conduct dialogue with the Sultanate of Oman to define the future administration and maritime services in the Strait of Hormuz...”

This point was widely understood to mean Iran would lift its blockade but still oversee and direct all traffic. When it exerted control of shipping traffic in March, Iran replaced the pre-war route that went down the center of the strait with one that guides traffic along Iran’s coast. However, after the MOU was signed, the Trump administration started instructing ships to use a different route, which passes through the territorial waters of Oman.

“We violated [the MOU] by setting up a southern corridor,” retired US Army Colonel Daniel Davis declared on his Deep Dive geopolitics podcast. “There’s nothing in the MOU that we signed that authorizes a southern corridor or America to enter into it and decide on our own how that’s going to be done. It’s just not there.” Davis, who returned from Afghanistan and blew the whistle in 2012 on civilian and military officials’ misleading of the public on how that war was progressing, suggested the US move in the strait was a deliberate provocation.

Deliberate or not, it was provocative indeed. After issuing radio warnings to ships attempting to use the southern route, Iran fired disabling shots at them. Trump then restarted his bombing of Iran, which prompted Iranian retaliation against American forces and the countries that host them. The two countries then began a long series of “tit for tat” strikes that continued into this week.

Then there’s Point 10 of the MOU, in which the Trump administration promised to issue sanctions waivers that would allow for unfettered Iranian exports of oil and petroleum. Trump revoked the waivers on July 7, pointing to Iran’s attacks on ships that didn’t submit to Iranian control of the Strait of Hormuz… control that, again, the United States seemingly agreed to under Point 5.

Numerically reflecting its high importance to Iran, Point 1 of the MOU required the “immediate and permanent termination of military operations on all fronts in Lebanon.” It focused not so much on Iran and the United States but more so “their allies” — the Iranian-allied Hezbollah militia and the US-allied State of Israel. However, Israel continued its operations, including a level of comprehensive destruction of civilian infrastructure in Southern Lebanon that mirrors what the Israeli Defense Forces did to Gaza. One can make the argument that the United States wasn’t in a position to impose MOU terms on Israel, but if that’s truly the case, Trump shouldn’t have signed an MOU by which he essentially certified that he would.

Doubling down, the Trump administration even took action to legitimize the IDF’s presence in Lebanon. “[The MOU] said we had to get the Israelis out of Lebanon. We made no effort to do that,” said former US ambassador to Saudi Arabia Chas Freeman. “In fact, we turned around and Marco Rubio went and…brokered an agreement between the Lebanese government and Israel that they will jointly go after Hezbollah. So what is this? At a minimum, it’s not very smart.”

Critically, Trump’s behavior bolsters the credibility of hardliners in the Iranian government who’ve repeatedly argued that the United States cannot be trusted and shouldn’t be negotiated with. Moderates prevailed over skeptical hardliners when Iran opted to sign the JCPOA, again when it twice attempted to seek sanctions relief and avert war via negotiations only to be subjected to surprise attacks, and again with the June 17 signing of the MOU.

Trump's actions have undercut the credibility of moderate Iranian leaders like President Pezeshkian, who ran on a platform favoring engagement with the West

Trump's actions have undercut the credibility of moderate Iranian leaders like President Pezeshkian, who ran on a platform favoring engagement with the West

“The hardliners said ‘don’t sign it, you can’t trust the Americans’,” Mearsheimer recently told Chris Hedges. “But the moderates prevailed, and then the hardliners proved to be correct, so they’re now in the driver’s seat, as best we can tell…and those hardliners will push forward a tougher deal for Trump to swallow” whenever the next version of an MOU is pursued.

It’s not only adversaries of the US government that have been subjected to Trump’s sudden reversals on terms he himself agreed to. Just ask Saudi Arabia.

On July 22, US Energy Secretary Chris Wright and Saudi energy minister Prince Abdulaziz bin Salman signed an agreement by which the kingdom would be able to build nuclear reactors and enrich uranium with US technology. Both governments published official announcements, and it was seen as a triumph for Saudi Crown Prince Mohammed bin Salman.

The very next morning, Trump blindsided the Saudis and his own subordinates, using a social media post to retroactively add a huge requirement — there would be no nuclear deal unless Saudi Arabia joined the Abraham Accords, which entails recognition of Israel as a legitimate state, and the establishment of official diplomatic relations.

Such a move would run counter to Saudi Arabia’s long-running insistence that recognition of Israel is unthinkable without a firm plan for Palestinian statehood. Further, Trump’s demand for a Saudi embrace of Israel comes at a time when Muslims within the kingdom and throughout the region are outraged by Israel’s destruction of Gaza and southern Lebanon, making such a move perilous for the Saudi royals. Contrary to the agreement his energy secretary had signed, Trump also suddenly declared there would be no enrichment of nuclear material inside Saudi Arabia.

“You strike a deal, you sign it, you announce it, you brag about it, and within 24 hours you’re changing the terms in a fundamental way,” observed the Quincy Institute’s Trita Parsi on Deep Dive. “If that’s what you do to Saudi Arabia — a country that the United States has a very close relationship with…on top of that, the Trump family has very close business ties with — then what are you going to do with Iran? What is the shelf life of any American commitment under Trump to the Iranians in any agreement?”

Or to anyone else, for that matter. “We’ve convinced the entire world that we don’t know what we’re doing, and we can’t be trusted, and we don’t keep our word, and we don’t even stay consistent from one day to the next,” former ambassador Freeman recently told Davis. “So how can you deal with us? That’s the question everybody has out there.”

As Alastair Crooke sees it, US diplomacy may never be the same. Summing up the effects of Trump’s multi-front assault on trust in America, the former British intelligence agent, diplomat and founder of the Beirut-based Conflicts Forum told Glenn Diesen, “The American ability to negotiate in the old-fashioned diplomatic idea, I think, is gone. I mean, we’re in a new era.”

Join thousands of free subscribers at starkrealities.net

* * *

Views expressed in this article are opinions of the author and do not necessarily reflect the views of ZeroHedge

Tyler Durden

Sat, 08/01/2026 - 23:20

Activist Carlos LeMar Dixon confronts Madison Police Chief John Patterson during a press conference about the shooting death of Corey Ruiz. / IMAGE: @CollinRugg via X

Activist Carlos LeMar Dixon confronts Madison Police Chief John Patterson during a press conference about the shooting death of Corey Ruiz. / IMAGE: @CollinRugg via X

Gen. Alex Grynkewich, source: US Air Force Senior Airman Spencer Perkins

Gen. Alex Grynkewich, source: US Air Force Senior Airman Spencer Perkins

A water tower in Plymouth, Minnesota, on Thursday after a cyberattack targeted the operating technology at more than 30 water systems across the state. (Ellen Schmidt/AP Photo/Ellen Schmidt)

A water tower in Plymouth, Minnesota, on Thursday after a cyberattack targeted the operating technology at more than 30 water systems across the state. (Ellen Schmidt/AP Photo/Ellen Schmidt)

Trump's actions have undercut the credibility of moderate Iranian leaders like President Pezeshkian, who ran on a platform favoring engagement with the West

Trump's actions have undercut the credibility of moderate Iranian leaders like President Pezeshkian, who ran on a platform favoring engagement with the West

Chinese People's Liberation Army (PLA) soldiers take part in military training at Pamir Mountains in Kashgar, northwestern China's Xinjiang region, on Jan. 4, 2021. STR/AFP via Getty Images

Chinese People's Liberation Army (PLA) soldiers take part in military training at Pamir Mountains in Kashgar, northwestern China's Xinjiang region, on Jan. 4, 2021. STR/AFP via Getty Images People's Liberation Army (PLA) soldiers take meteorological observation training in Jinan, Shandong Province of China, on May 29, 2016. Getty Images

People's Liberation Army (PLA) soldiers take meteorological observation training in Jinan, Shandong Province of China, on May 29, 2016. Getty Images

Recent comments