Exporters Still Are Not Eating the Trump Tariffs: They are Taxes on Us

The post Exporters Still Are Not Eating the Trump Tariffs: They are Taxes on Us appeared first on CEPR.

Speak Your Mind 2 Cents at a Time

The post Exporters Still Are Not Eating the Trump Tariffs: They are Taxes on Us appeared first on CEPR.

Authored by Guy Birchall via The Epoch Times,

An Italian court sentenced 32 people to a total of more than 170 years in prison on July 16, over their role in a 2018 bridge collapse that claimed the lives of 43 people.

The collapsed Morandi Bridge in Genoa, Italy, on Aug 14, 2018. Reuters/Stefano Rellandini

The collapsed Morandi Bridge in Genoa, Italy, on Aug 14, 2018. Reuters/Stefano Rellandini

The former head of Italian motorway operator Autostrade per l'Italia (ASPI), Giovanni Castellucci, received the longest sentence of 12 years in prison for his role in the disaster, which saw the Morandi motorway bridge near the city of Genoa fall apart during a rainstorm on the morning of Aug. 14, 2018.

Michele Donferri Mitelli, another former senior manager at the publicly traded motorway management company, was given an 11-year sentence, with a further 30 defendants receiving custodial sentences.

Others sentenced included managers and engineers from ASPI's engineering subsidiary SPEA, as well as former officials from Italy's Infrastructure and Transport Ministry.

Of the 57 people who stood trial, a further 25 were either acquitted or cleared due to the statute of limitations, Italian outlet La Repubblica reported.

The Genoa courtroom fell silent as presiding judge Paolo Lepri read the verdicts for around 45 minutes, with 400 relatives of the victims, lawyers, journalists, and members of the public listening, Reuters reported.

Egle Possetti, president of the Committee for the Remembrance of the Morandi Bridge Victims, called the verdicts "important" and "positive."

"We believe the judges have done a thorough job, examining each position in detail," she told Italian public broadcaster RAI.

"We are pleased that responsibility has been acknowledged in all three areas of prosecution, that is, by ASPI, by SPEA, and by the ministry," said Possetti, who lost her sister, brother-in-law, and her sister's two children in the collapse.

The verdicts, however, are subject to appeal, with Castellucci, who also served as CEO of Atlantia, the controlling shareholder in ASPI at the time, planning to do so.

He was convicted of complicity in multiple counts of manslaughter through negligence, with prosecutors asking for a sentence of more than 18 years, rather than the 12 years he was eventually given, RAI reported.

Castellucci is already in prison, serving a six-year sentence over another fatal incident in 2013 on a viaduct in southern Italy, and was not in court to hear the verdict, but his legal team said they would appeal and that he had been made a scapegoat.

His lawyers, Giovanni Paolo Accinni and Guido Carlo Alleva, said they are "ready to appeal" the sentence, saying they believe their client "could not and should not have been convicted."

"We will read the reasons. We are convinced of Castellucci's innocence, but the trial doesn't end here. Criminalizing company CEOs is unfair; Castellucci is already in prison for this. And so is another CEO who bears no guilt," they said, according to Genoese outlet Il Secolo XIX.

The other CEO they are referring to is the former CEO of Ferrovie dello Stato and RFI, Mauro Moretti, who is currently serving a five-year sentence relating to a 2009 rail disaster in Viareggio, Tuscany, which killed 32 people.

Under the Italian legal system, the ruling of the first instance can be appealed at least twice.

Following the sentencing, Possetti said that "the new battle begins to succeed in having this ruling confirmed on appeal and above all to delegitimize any attempt to provide additional protection to managers, who should be subject to the law like the rest of us," Il Secolo XIX reported.

The CollapseThe collapse of the Morandi bridge in August 2018 stunned Italy and sparked years of investigations into the management and maintenance of its aging infrastructure.

A 650-foot portion of the bridge collapsed, plunging 160 feet onto a riverbed, a railway, and two warehouses, while as many as 35 vehicles were driving across it.

The disaster sparked a dispute between Atlantia, controlled by the Benetton family, and the Italian government, which eventually culminated in the sale of Atlantia's controlling stake in ASPI.

Prosecutors argued that years of poor maintenance, ignored warning signs, and delayed improvement works contributed to the collapse, saying that vital repairs were postponed while profits continued to be pocketed.

The prosecutors' argument was backed up by a 2020 expert report into the disaster, which said the collapse was triggered by the rupture of corroded steel cables inside one of the stay cables on the southern side of pile 9, Italian outlet IVG reported that year.

A "pile," known as a "pier" in the United States, is a vertical concrete structure that supports the weight of the bridge deck above it.

The corrosion of the prestressing strands within pile 9 had progressed over decades due to the ingress of water and oxygen, according to the report, which concluded that the root cause was long-term inadequate maintenance and insufficient inspections by ASPI and its subsidiary Spea.

It found that proper controls and maintenance interventions, if properly implemented, would have had a high probability of preventing the collapse. The report also noted that warnings and recommendations made by the bridge's original designer, Riccardo Morandi, regarding corrosion risks had been progressively neglected over the years.

The defense teams rejected this theory, saying that the disaster was caused by an original design defect in the bridge's stay cable in pile 9, which failed, and that no maintenance program could have prevented the collapse.

Tyler Durden Sat, 07/18/2026 - 08:10Finnish MEP Sebastian Tynkkynen has warned that Britain is fast becoming the worst example in Europe when it comes to defending free speech after he became the latest elected European politician to be banned from entering the country ahead of his appearance at the inaugural Conservative Political Action Conference (CPAC) Great Britain.

In a video posted on social media, the conservative politician said, “I was just banned from entering the U.K. I am an elected member of the European Parliament and was invited to speak at the very first conservative CPAC conference in the U.K.

“We had the adverts out, flights and hotel booked, and I was supposed to head to the airport in just two hours.

“Then, only moments ago, I was informed that my presence wouldn’t be conducive to the public good.

“Throughout my political career, I have defended our girls and women from the threats posed by mass migration. For some, like U.K. Prime Minister Keir Starmer, this is hate speech.

“For me, it is simply what all politicians should be doing: addressing the problem, changing the legislation and sending them home.”

Tynkkynen then warned the British people that something is “deeply wrong” with their country, and that it was “becoming the worst example in Europe of the death of freedom of speech.”

"Dear British People, something is deeply wrong with your country. You are becoming the worst example in Europe of the death of free speech."

— Remix News & Views (@RMXnews) July 16, 2026

Finnish conservative @SebastianMEP reveals he is the latest elected politician to be banned from entering Britain on the eve of #CPACUK,… pic.twitter.com/Q73a2dwtGQ

He urged them to change their leadership if they wanted to change their lives “for the better.”

Tynkkynen is a member of the co-governing Finns Party, a right-wing populist party that is currently the second-largest in the Finnish parliament. The party holds seven of the 19 ministerial positions in Prime Minister Petteri Orpo’s coalition government.

He is also a member of the European Conservatives and Reformists Group (ECR), the European parliamentary faction originally founded by the U.K. Conservative Party when Britain was still a member of the European Union.

Tynkkynen is the latest in a growing list of European and US politicians and political commentators to be banned from Britain after the Home Office deemed their conservative views not to be “conducive to the public good.”

This is the phrase used by the U.K. government in notices handed to individuals when they are informed that their Electronic Travel Authorisation (ETA) has been revoked.

In May, Polish MEP Dominik Tarczyński vowed to sue U.K. Prime Minister Keir Starmer personally after the Home Office cancelled his permission to travel to Britain ahead of a major patriotic rally in London.

“This is what communism looks like in the 21st century,” Tarczyński said.

“Starmer will be sued by me. Not the government, not the Home Office, but Starmer personally. Once you lose the next election, communist, we’ll meet in court!” the conservative politician added.

Other figures banned ahead of speaking at the London rally back in May included Dutch conservative activist Eva Vlaardingerbroek, US commentator Joey Mannarino, MAGA influencer Valentina Gomez and Spanish political commentator Ada Lluch.

Tyler Durden Sat, 07/18/2026 - 07:00The weekend is here! Pour yourself a mug of Danish Blend coffee, grab a seat outside, and get ready for our longer-form weekend reads:

• The American E.V. Has Been Crushed. Will It Take the U.S. Auto Industry With It? The largest U.S. automakers have backed away from electric vehicles, even as global sales are booming. The decision may make them obsolete. (New York Times)

• AI is changing what we can do. Who we become is still our choice: To understand AI’s effect on moral character, ethicist Kwame Anthony Appiah goes back to John Stuart Mill, and the idea that people are shaped by their choices. (Humanist Review) see also AI isn’t destroying entry-level jobs. It’s changing them: Here are the ways leading companies are already responding to the AI revolution in professional services. (Financial Times)

• From Hong Kong to Xiānggǎng: The Hong Kong of old is over. Go to Xiānggǎng and see for yourself. Stephen Roach on Hong Kong’s transformation into Xiānggǎng — the slow-motion absorption of a once-global city. (Conflict Stephen Roach)

• Shooting Starlink: The “no limits” partnership between Russia and China is taking aim at Elon Musk: Secret documents from a series of clandestine Russian-Chinese military forums reveal a joint plan to defeat Elon Musk’s Starlink and a weapons development partnership far deeper than either country will admit. From air- and missile-defense systems to AI-enhanced drone capabilities, cooperation between Moscow and Beijing is allowing Russian forces to keep pace with Ukrainian innovations while China gains the opportunity to test its wares under combat conditions. Although the threat of increased Western sanctions continues to place constraints on their “no limits” partnership, Russia and China are moving forward with several joint projects — and former U.S. military officers are concerned about Washington’s will to stop them. (The Insider)

• What Even Is Ultraprocessed Food? It’s less a useful label and more of a vibe. One of the biggest boogeymen around these days is ultraprocessed food. You can see dozens if not hundreds of news articles every week decrying the damage that these foods are doing to our health. UPFs are apparently responsible for everything from dementia to heart disease and virtually every other health problem in between. They’re so bad that the U.S. Food and Drug Administration is considering “taking action” against UPFs to stop Americans from eating them. (Slate)

• The Lost Joy of Music Piracy: What.CD, Oink, and the banalities of streaming. As an avid pirate suddenly finding himself in the midst of the music business, Sheridan saw the issue from a different angle than most of the suits he was surrounded by. “I got brought in and we were being flown to New York, the label was taking us out to these expensive dinners and paying for everything—top notch hotels, everyone had private cars and drivers. There was so much money going around, and it wasn’t the artists who were rolling in cash. I remember one of my first comments to Trent [Reznor] was, ‘Now I see why CDs cost 18 dollars.’” (Pigeons & Planes)

• What will be left for us to work on? A thoughtful essay on the shrinking frontier of human-only work as AI capabilities expand. The question isn’t whether machines will take jobs — it’s whether the jobs that remain will be worth doing. My keynote at ICML 2026 (AI As Normal Technology)

• Winners of the International Aerial Photographer of the Year: Stunning images from above — the kind of photography that makes you reconsider what the world actually looks like when you’re not standing on it. A collection of winners and selected images from the competition’s “Top 101” grouping, chosen from more than 1,500 entries by professional and amateur aerial photographers around the world (The Atlantic)

• The 25 most influential works of American culture: A decade-by-decade look at the books, music, art and ideas that shaped society. The Washington Post’s interactive ranking — across music, literature, film, TV, and art. The list will start arguments, which is the point. (Washington Post)

• The bitter history of England vs Argentina, a World Cup semi-final steeped in bad blood: Maradona’s Hand of God, Beckham’s red card, the Falklands — every England-Argentina match carries the weight of decades of grudge. The Athletic previews the latest chapter. (The Athletic)

Video of the day: Does Anyone Know the Real Mick Jagger? He’s Not So Sure

Be sure to check out our Masters in Business this weekend with Jason Wenk, founder and CEO of Altruist, a modern custodian built as a clean sheet from the ground up, fully integrated with artificial intelligence. He began his career at Morgan Stanley before launching Retirement Wealth Advisors, and then FormulaFolios. The through-line of his career has been creating lower-cost, tech-enabled, financial advice.

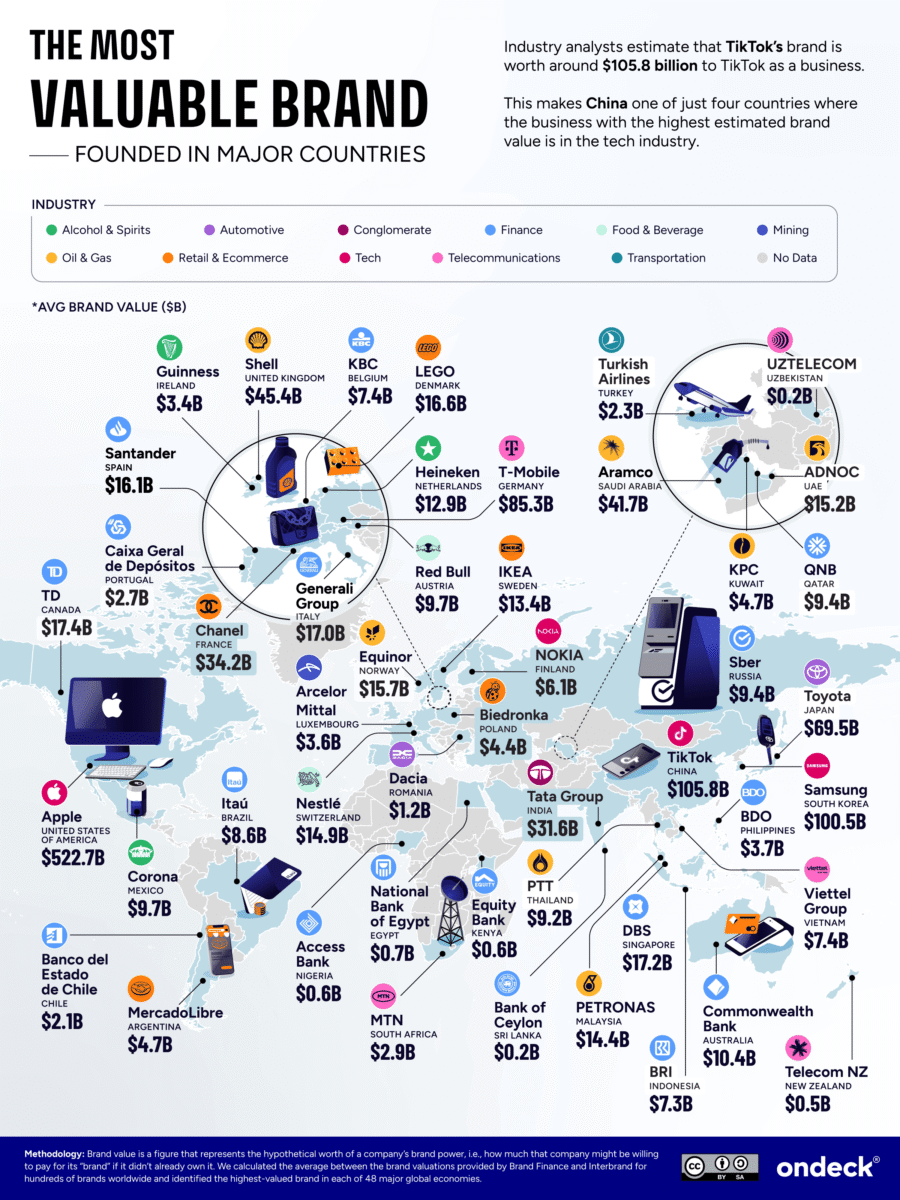

The Most Valuable Brands in the World

Source: On Deck

Sign up for our reads-only mailing list here.

~~~

To learn how these reads are assembled each day, please see this.

The post 10 Weekend Reads appeared first on The Big Picture.

There are stories that announce themselves with explosions, riots, or breaking-news headlines, and then there are stories so subtle that they quietly rewrite an entire society before anyone realizes what has happened. This is one of those stories. During the preparation of this investigation, several retired police officers, private security professionals, emergency responders, and ordinary citizens described nearly identical experiences despite living hundreds or even thousands of miles apart. None believed they were witnessing anything extraordinary at first. It was only when they looked backward—sometimes over a decade—that a disturbing pattern became impossible to ignore. Streets had not become military checkpoints overnight. Neighborhoods had not suddenly filled with surveillance towers. Instead, the changes arrived one camera, one drone, one security contract, and one "temporary" emergency measure at a time until extraordinary security became indistinguishable from ordinary life. What follows is not an argument against public safety, nor an attempt to romanticize a past that was hardly free from crime or violence. It is an examination of a transformation that has occurred quietly enough for most people to stop seeing it altogether.

There is an old saying among investigators that people rarely notice change while it is happening. They notice it only when they compare today's reality with memories that have remained frozen in time. Memory preserves snapshots, while history moves continuously. That disconnect explains why so many citizens insist that nothing fundamental has changed even as the physical landscape around them becomes increasingly populated by surveillance cameras, armed guards, automated license plate readers, biometric scanners, drones, and predictive security technologies. No single installation appears revolutionary. No single policy seems capable of altering the character of a society. Yet history rarely advances through dramatic leaps. More often, it advances through thousands of small decisions that seem perfectly reasonable when viewed independently but become historically significant when examined collectively.

The quiet militarization of civilian spaces represents precisely this kind of transformation. Unlike traditional militarization, which is associated with soldiers, armored vehicles, and visible state authority, the contemporary version is largely administrative, technological, and commercial. It emerges through contracts signed by private security companies, insurance requirements imposed upon businesses, municipal investments in surveillance infrastructure, advances in artificial intelligence, and a public increasingly willing to exchange greater visibility for greater security. The result is not a police state in the conventional sense, nor is it a society living under constant emergency. Instead, it is something considerably more complex: an environment in which observation has become routine, data has become a form of infrastructure, and security has evolved into a permanent layer of everyday life.

Perhaps the most remarkable aspect of this evolution is not the technology itself but the speed with which human beings adapt to its presence. Psychological research has repeatedly demonstrated that people rapidly normalize environmental changes once those changes become familiar. The camera that initially attracted attention soon becomes part of the background. The security guard stationed near the supermarket entrance eventually disappears into peripheral vision. The drone hovering above a community festival is no longer perceived as unusual after it has appeared several times. Familiarity breeds acceptance far more effectively than persuasion ever could. This gradual normalization explains why discussions surrounding surveillance often occur only after new technologies have already become deeply embedded within public life.

I remember a conversation several years ago with a retired emergency management coordinator who had spent more than three decades working alongside law enforcement agencies during natural disasters and large public events. He was not particularly interested in politics, nor did he express hostility toward modern security practices. What struck me instead was the simplicity of his observation. "When I started," he said while looking across an ordinary shopping center parking lot, "the only people carrying radios and wearing body armor were police officers responding to emergencies. Now look around." At first, I assumed he was exaggerating. Then I began counting. Private security personnel equipped with ballistic vests. Cameras mounted on nearly every light pole. Delivery vehicles fitted with multiple recording systems. Police drones deployed during missing-person searches. Automatic barriers controlling access to residential developments. It was difficult to identify the precise moment when these features had become ordinary because none of them had arrived simultaneously.

That conversation stayed with me, not because it revealed a hidden conspiracy but because it exposed something much more subtle. Societies rarely recognize structural change while they are living through it. They recognize it only after the new normal has replaced the old one so completely that remembering life before the transition begins to feel almost nostalgic. Consider the average suburban neighborhood in the United States twenty-five years ago. Most homes lacked internet-connected cameras. Private security patrols were relatively uncommon outside affluent gated communities. Drones existed primarily as military technologies unfamiliar to the general public. License plate recognition systems were largely confined to specialized law enforcement operations. Today, many of those same neighborhoods contain dozens of privately owned surveillance devices, neighborhood watch applications, cloud-connected doorbell cameras, automated traffic monitoring systems, and security contractors who operate with increasing sophistication. None of these developments occurred through a single national directive. They accumulated gradually until they became invisible.

The numbers alone tell only part of the story. What matters far more is the psychological environment these technologies create. Human behavior changes when observation becomes continuous, even when the observers remain anonymous or the collected data is never actively reviewed. Sociologists have long argued that visibility influences conduct because people instinctively modify their actions when they believe they are being watched. The effect is often subtle rather than dramatic. Individuals spend less time lingering in certain locations, become more cautious about spontaneous interactions, and unconsciously adapt their routines to environments where cameras, sensors, and digital records are omnipresent. Most of these behavioral adjustments occur without deliberate reflection, making them difficult to recognize despite their cumulative significance.

The transformation is particularly striking because it extends well beyond government institutions. Much of today's surveillance infrastructure belongs to private corporations, residential associations, logistics companies, retailers, hospitals, universities, and homeowners. This decentralized architecture creates an ecosystem in which observation is distributed rather than centralized. A person traveling only a few miles through an ordinary town may appear on hundreds of independently operated cameras before reaching their destination. None of those systems alone possesses complete knowledge of that individual's activities. Collectively, however, they generate an extraordinarily detailed record of movement, timing, and behavior that would have been almost unimaginable only a generation ago.

For most people, this reality inspires little concern because everyday life continues to function normally. Children still attend school, families still gather in parks, commuters still stop for coffee on the way to work, and neighbors still walk their dogs after sunset. The absence of visible crisis creates the impression that surveillance is merely another technological convenience, comparable to smartphones or GPS navigation. Yet history suggests that infrastructure built for one purpose frequently acquires additional functions over time. Roads designed for commerce become strategic military assets during war. Communication networks developed for business become indispensable during emergencies. Surveillance systems installed to discourage theft gradually become valuable tools for investigations, crowd management, disaster response, insurance litigation, and behavioral analysis. Technology rarely remains confined to its original purpose once society discovers broader applications.

That observation is neither cynical nor alarmist. It is simply a recurring pattern throughout modern history. Every generation inherits technologies whose long-term consequences become fully apparent only decades after their introduction. The internet began as a communication platform before becoming the foundation of global commerce and social interaction. Smartphones evolved from portable telephones into devices capable of documenting nearly every aspect of human behavior. Artificial intelligence, once limited to research laboratories, now assists financial institutions, healthcare providers, military planners, and security agencies alike. Surveillance technologies are following a remarkably similar trajectory. What initially appeared to be isolated security improvements increasingly resembles an interconnected ecosystem whose influence extends far beyond crime prevention alone.

1. Everyday Spaces Are No Longer What They Used to BeThe easiest way to understand how profoundly everyday life has changed is not by reading crime statistics or studying government reports, but by remembering what an ordinary afternoon looked like twenty or thirty years ago. You could stop at a neighborhood gas station, pay in cash, exchange a few words with the cashier, and continue your day without leaving much behind except a receipt that would probably disappear into a drawer. Today that same five-minute stop may generate dozens of digital records. Your vehicle is captured entering the parking lot, your license plate may be scanned automatically, your payment creates a financial record, your smartphone silently exchanges location data with multiple applications, and security cameras document your movements from several angles. None of these actions feels extraordinary because each one has become part of the invisible architecture of modern life.

What fascinates me most is not the technology itself but how effortlessly people have adapted to it. Years ago, a newly installed camera outside a small grocery store would become a topic of conversation. Customers would ask why it had been installed or whether crime in the area had increased. Today another camera appears, then another, followed by upgraded lighting, automated doors, and perhaps a security guard standing quietly near the entrance. Few people ask questions anymore. The additions blend into the background until they become as ordinary as shopping carts or parking spaces. That silent acceptance may be one of the defining characteristics of our era.

I was reminded of this during a conversation with the owner of a family-run hardware store in the Midwest. His business had operated for decades without armed security, and for years he resisted installing additional surveillance because he believed it sent the wrong message to customers. Eventually, repeated thefts forced his hand. First came two cameras. Then eight. A year later he hired an evening security officer. "Nothing happened overnight," he told me. "Every decision made sense at the time. But when I look around now, this doesn't feel like the same store my father built." His words were less a complaint than a quiet acknowledgment that necessity often changes institutions long before anyone notices their identity has changed.

That story reflects something larger than one business owner's experience. The quiet militarization of civilian spaces has rarely been driven by dramatic political declarations. Instead, it has emerged through countless practical decisions made by people trying to solve immediate problems. Retail theft rises, so cameras multiply. Violent incidents receive national attention, so schools expand security protocols. Residential burglaries increase, so neighborhoods invest in automated gates and patrol vehicles. Each decision appears rational in isolation. Yet viewed together, they reveal a society steadily constructing an infrastructure of permanent vigilance.

2. The Surveillance Economy Nobody Really NoticedMost public conversations focus on government surveillance, but that discussion often overlooks where the largest expansion has actually occurred. Today, private companies collect extraordinary amounts of information simply because data has become one of the world's most valuable economic resources. Shopping habits, travel routines, online purchases, vehicle movements, loyalty programs, smart home devices, delivery services, and mobile applications all contribute pieces to an increasingly detailed picture of everyday life. Much of this information is gathered not because someone is personally interested in any individual, but because aggregated behavioral data has become commercially valuable.

That distinction matters. Modern surveillance is rarely the product of a single centralized observer watching everyone simultaneously. Instead, it resembles thousands of overlapping mirrors, each reflecting a small portion of reality. A retailer wants to understand customer behavior. A navigation app wants traffic information. An insurance company wants to assess risk. A logistics company wants to optimize deliveries. A homeowner wants to know who approached the front door. Individually, these objectives appear reasonable. Collectively, however, they create a remarkably detailed digital ecosystem capable of reconstructing daily routines with surprising accuracy.

Several cybersecurity analysts have described this phenomenon using an analogy that stayed with me long after I first heard it. Imagine dropping a handful of puzzle pieces onto a table. One piece tells almost nothing. Ten pieces reveal very little. But eventually enough fragments accumulate for the entire picture to emerge without anyone intentionally assembling it from the beginning. Modern surveillance works much the same way. Rarely does one camera or one database reveal everything. The picture becomes visible only after countless independent systems begin recording the same individual from different perspectives.

Perhaps the most unsettling consequence is that many people continue believing privacy disappears only when someone actively watches them. In reality, observation is increasingly passive. Information is collected first because storage is inexpensive, processing power is abundant, and future usefulness cannot always be predicted. Only later, if circumstances require it, does someone search the archive. This subtle reversal—from collecting information because it might become useful rather than because it already is—represents one of the most significant yet least discussed shifts in modern security philosophy.

3. Cameras Rarely Prevent History—They Record ItOne misconception persists despite decades of technological progress: the belief that more cameras automatically produce greater safety. Experience suggests a far more complicated reality. Cameras excel at documenting events, reconstructing timelines, identifying suspects, and supporting investigations. They provide evidence. What they cannot consistently do is intervene during the critical first moments when violence, accidents, or panic unfold. History is filled with incidents that occurred under extensive surveillance, reminding us that observation and prevention are not interchangeable concepts.

A retired detective once explained this distinction in a way that has stayed with me ever since. "People think cameras stop crime," he said. "Most of the time, they help explain what happened after it's over." His comment was not intended as criticism of surveillance technology. On the contrary, he considered modern investigative tools indispensable. What concerned him was the growing tendency for communities to confuse documentation with security itself. Recording an emergency and preventing an emergency require fundamentally different capabilities.

That misunderstanding occasionally produces a false sense of confidence. A parking garage filled with cameras may appear secure while remaining poorly lit or inadequately staffed. A neighborhood equipped with sophisticated surveillance may still suffer from slow emergency response times or declining social cohesion. Visible technology often reassures the public because it symbolizes action, even when the underlying causes of insecurity remain unresolved. This is not an argument against surveillance but a reminder that technology cannot substitute for strong communities, effective policing, responsible urban planning, and individual awareness.

Perhaps that explains why experienced emergency responders rarely rely on any single protective measure. They lock doors despite alarm systems. They identify exits despite emergency lighting. They remain aware of their surroundings despite cameras covering the area. Experience teaches an uncomfortable lesson: technology performs best when it complements human judgment rather than replacing it.

4. The Sky Is No Longer EmptyFor generations, privacy possessed a vertical dimension that few people consciously considered. Fences blocked the view from the street, trees created natural barriers, and distance itself provided a degree of practical anonymity. Unless someone climbed a hill or chartered an aircraft, many private activities remained largely invisible from above. Drones have fundamentally altered that assumption, not through dramatic military operations but through their quiet integration into civilian life.

Fire departments deploy them to monitor wildfires. Search-and-rescue teams use them to locate missing hikers before darkness falls. Utility companies inspect power lines. Farmers survey crops. Police departments reconstruct accident scenes within minutes instead of hours. Journalists capture footage of natural disasters impossible to obtain from the ground. These are legitimate and often life-saving applications that demonstrate why drone technology has spread so rapidly across both public and private sectors.

Yet every useful technology introduces questions extending beyond its original purpose. A device capable of finding a lost child is equally capable of observing neighborhoods from perspectives that previous generations rarely imagined. Again, the issue is not whether drones are inherently beneficial or harmful. Like most technologies, they are neither. The more interesting question concerns how quietly they have changed our expectations of what constitutes normal observation. Ten years ago, a drone hovering above a suburban neighborhood would have attracted curious neighbors. Today many people glance upward, recognize the familiar sound, and continue walking without another thought.

That normalization may ultimately prove more significant than the technology itself. Human beings adapt remarkably quickly to persistent environmental change. Once something becomes familiar, we stop asking why it appeared in the first place. History suggests that this tendency toward normalization often shapes societies far more profoundly than any single invention ever could.

5. Armed Security Is Becoming Part of the Civilian LandscapeNot long ago, seeing an armed security officer outside a neighborhood supermarket would have prompted questions. Had there been a robbery? Was someone important expected to visit? Had violence occurred nearby? Today, in many parts of the United States, that same sight barely interrupts a shopper's routine. People push their carts past ballistic vests, body cameras, portable radios, and duty belts with the same indifference they reserve for shopping baskets or self-checkout kiosks. The visual language of security has quietly changed, and with it, the psychological atmosphere of places that once felt entirely civilian.

Private security has grown into an industry that now performs functions once associated almost exclusively with public law enforcement. Hospitals maintain dedicated security divisions, universities employ sworn officers alongside private contractors, residential developments operate twenty-four-hour patrols, and retail chains increasingly invest in highly trained personnel capable of responding to violent incidents before police arrive. The reasons behind these decisions are rarely ideological. Rising theft, liability concerns, staffing shortages, and the unpredictable nature of modern emergencies have convinced many institutions that waiting for outside assistance is no longer sufficient. Preparedness has become a business requirement rather than an optional precaution.

One former security director explained the shift in remarkably practical terms. "People think we're preparing for the worst every day," he told me. "The reality is much simpler. We're preparing for the possibility that one day won't be ordinary." That distinction matters because it illustrates how security professionals themselves often view their role. They are not expecting society to collapse tomorrow. They are responding to a world in which low-probability, high-impact events have become difficult to ignore. Schools prepare for emergencies they hope never occur. Hospitals train for scenarios they may encounter only once in a decade. Shopping centers review active-threat procedures despite spending most days dealing with lost children and shoplifting.

Yet there is another side to this evolution that receives far less attention. Visible security changes how people interpret the spaces around them. Even when no danger exists, the presence of armed personnel subtly communicates that danger is possible. Over time, communities begin recalibrating their expectations. What once appeared extraordinary gradually becomes ordinary, and future generations inherit a definition of "normal" that differs significantly from the one their parents knew. Few people consciously recognize this adjustment while it is happening, but history suggests that changes in public psychology often outlast the circumstances that originally produced them.

6. The Most Valuable Information Is the Information People VolunteerIf surveillance cameras reveal where people go, digital technology increasingly reveals who they are. Modern life is built upon convenience, and convenience almost always leaves a trail. Smartphones document movement, online purchases reveal preferences, streaming services record interests, fitness watches monitor physical activity, connected vehicles collect operational data, and social media platforms encourage individuals to broadcast fragments of their daily lives voluntarily. Rarely is anyone forced to disclose this information. More often, people exchange it willingly for speed, personalization, entertainment, or efficiency.

The irony is difficult to ignore. Discussions about privacy frequently focus on sophisticated surveillance technologies while overlooking the extraordinary amount of personal information people publish themselves. A photograph celebrating a new generator may unintentionally reveal the layout of a garage. A vacation post announces an empty house to anyone paying attention. A casual video filmed in the backyard can expose security cameras, storage sheds, expensive tools, or routines repeated week after week. None of these details seems particularly significant on its own. Together, however, they create a remarkably complete portrait of a household.

Years ago, I met a cybersecurity consultant who specialized in corporate risk assessments. Instead of beginning his presentations with discussions of hacking software or encrypted networks, he projected publicly available social media posts collected from volunteers in the audience. Within minutes, he had identified home addresses, vehicle models, children's schools, frequent travel destinations, and daily routines using nothing more than information people had shared themselves. The room became noticeably quieter. "I didn't hack anyone," he said. "You introduced yourselves before I walked in."

That demonstration has remained with me because it illustrates a broader truth about the modern information environment. The greatest vulnerability is often not sophisticated technology but ordinary human behavior. Effective operational security rarely begins with encryption or expensive equipment. More often, it begins with asking a remarkably simple question before pressing "post": does the entire world really need to know this? The answer is frequently no, yet contemporary culture often rewards visibility far more enthusiastically than discretion.

7. The Low-Profile AdvantageAmong experienced emergency planners, there is an old principle that receives surprisingly little attention outside professional circles: the individual who attracts the least unnecessary attention often preserves the greatest number of options. This concept has nothing to do with secrecy or distrust of society. Instead, it reflects a practical understanding that visibility creates expectations, while anonymity preserves flexibility. In stable times, that difference may appear insignificant. During periods of uncertainty, it can become remarkably important.

Popular culture has transformed preparedness into a highly visible identity. Social media platforms are filled with tactical equipment reviews, warehouse-sized food storage tours, customized vehicles covered in survival-themed decals, and endless discussions about worst-case scenarios. While much of this content is educational or entertaining, it also illustrates how preparedness has increasingly become something performed before an audience rather than practiced quietly at home. Ironically, the desire to demonstrate readiness sometimes undermines the very resilience individuals hope to achieve.

I once asked a man who had spent decades working in disaster logistics why his own preparations appeared so remarkably ordinary. His answer was immediate. "Because normal people are rarely remembered." He drove an unremarkable vehicle, maintained a conventional-looking property, and purchased supplies gradually over many years. Nothing about his appearance suggested that he had invested significant time thinking about resilience. That, he explained, was entirely intentional. "Looking ordinary isn't pretending. It is understanding that attention is a resource you shouldn't waste."

Perhaps that philosophy has become more relevant than ever before. In an age where digital records, surveillance systems, and online visibility intersect continuously, resilience depends not only on what individuals possess but also on how predictably they present themselves to the world. Quiet competence rarely generates headlines, but history repeatedly suggests it endures long after louder performances fade.

8. Teaching Awareness Without Creating FearEvery generation inherits a different understanding of risk. Children growing up today will likely consider cameras in classrooms, facial recognition at airports, drone footage on local news broadcasts, and digital identity verification as ordinary features of life rather than technological milestones. Their perception of privacy will inevitably differ from that of previous generations, not because they value freedom less, but because they have never experienced a world where continuous connectivity did not exist.

The challenge for parents, educators, and communities is therefore remarkably delicate. Teaching awareness should never become synonymous with teaching fear. Children benefit from understanding why oversharing online carries consequences, why location data deserves careful management, and why respectful interactions with security personnel matter. They do not benefit from believing they live under constant threat or surveillance by unseen forces. Fear narrows judgment; awareness expands it.

A former school administrator offered an observation that deserves wider attention. "We spent years teaching children not to talk to strangers," she said. "Now we have to teach them not to introduce themselves to millions of strangers without realizing it." Her comment captured the extraordinary shift that has occurred within a single generation. The greatest changes in personal security are no longer confined to physical spaces. Increasingly, they unfold through screens small enough to fit into a pocket.

Families that cultivate calm observation rather than constant anxiety often develop stronger resilience as a result. They notice exits without becoming paranoid. They recognize unusual behavior without assuming everyone represents a threat. They value privacy without withdrawing from society. That balance may prove one of the most important skills the coming decades will demand. It is easy to become frightened by a changing world. It is considerably harder—and ultimately far more valuable—to understand it clearly without allowing fear to distort judgment.

9. Security Theater or a Necessary Evolution?At some point, every serious discussion about surveillance reaches the same uncomfortable question: are we witnessing an unavoidable adaptation to a more complex world, or have we slowly accepted a level of monitoring that previous generations would have considered excessive? The answer is almost certainly more complicated than either side is willing to admit. Those who argue that expanded security is entirely justified can point to terrorism, organized retail crime, cyberattacks, mass shootings, and increasingly sophisticated criminal networks. Those who worry about surveillance can point to the steady erosion of anonymity, the commercialization of personal data, and the tendency of emergency measures to outlive the emergencies that inspired them. Both observations can be true simultaneously, which is precisely what makes the conversation so difficult.

History offers surprisingly few examples of societies voluntarily abandoning security technologies once they become normalized. Metal detectors introduced after periods of heightened threat rarely disappear. Temporary surveillance measures frequently become permanent infrastructure. Databases expand because additional information is almost always perceived as useful, even if its immediate purpose is unclear. Institutions, whether public or private, naturally prefer retaining capabilities rather than surrendering them. From an operational perspective, this makes perfect sense. From a civic perspective, however, it raises important questions about how societies define proportionality, accountability, and the limits of observation.

One constitutional scholar I interviewed years ago summarized the dilemma with remarkable simplicity. "The debate usually begins too late," he said. "By the time people start asking whether a technology should exist, it has already become indispensable." Looking back, his observation feels less like political commentary and more like a recurring lesson in technological history. Society rarely debates inventions before they arrive. Instead, it debates their consequences after they have become woven into daily life. Smartphones, social media, facial recognition, artificial intelligence, and drone technology all followed remarkably similar trajectories. Widespread adoption consistently outpaced public reflection.

That delayed reflection explains why surveillance often generates polarized debates that produce little genuine understanding. Public conversations tend to frame the issue as a choice between complete security and complete privacy, despite the fact that neither condition has ever truly existed. Every functioning society requires some degree of security infrastructure, just as every free society depends upon meaningful limits governing how power is exercised. The challenge is not choosing one principle over the other but preserving both as technological capabilities continue expanding faster than legal, ethical, and cultural norms can adapt.

Perhaps the greatest danger lies not in surveillance itself but in intellectual complacency. When people stop asking why new systems are introduced, who controls them, how information is stored, or what safeguards exist against misuse, public oversight quietly weakens. Democracies depend upon informed citizens capable of distinguishing reasonable security measures from unnecessary excess. That responsibility cannot be delegated entirely to governments, corporations, or technology companies. It belongs, ultimately, to the society that accepts—or questions—them.

10. The Future Arrived Without Asking PermissionThe most profound historical transformations rarely resemble the dramatic scenes portrayed in films. They unfold through ordinary mornings, routine errands, software updates, budget approvals, infrastructure projects, and countless administrative decisions that appear insignificant when viewed individually. Few people remember the day the first camera appeared in their neighborhood. Even fewer remember when the second, third, or twentieth was installed. Yet collectively those moments changed the environment in which millions now live.

Looking back across the past two decades, it becomes remarkably difficult to identify a single turning point because there wasn't one. There was no announcement declaring that civilian life had entered an era of persistent observation. No legislation instructed citizens to become comfortable with drones overhead or private security officers carrying patrol rifles in commercial districts. The transition occurred through accumulation rather than revolution. Every response addressed a genuine concern. Every improvement solved a practical problem. Together, they reshaped the expectations of an entire generation.

Perhaps that explains why older emergency managers, retired police officers, and longtime journalists often describe the same feeling despite coming from completely different professions. None of them argues that modern society should abandon technology or ignore legitimate threats. What they notice instead is something subtler: the pace at which exceptional security measures become ordinary social architecture. Once familiarity takes hold, memory begins to fade. Younger generations inherit systems that appear timeless despite being remarkably recent additions to everyday life.

For individuals committed to preparedness, this changing landscape demands neither paranoia nor political tribalism. It demands literacy—an ability to understand how security systems function, where technology genuinely improves public safety, where personal privacy deserves thoughtful protection, and how digital habits increasingly shape real-world resilience. Quiet preparedness has never been about hiding from society. It has always been about understanding reality before reality forces understanding upon you.

That may be the defining lesson of this century. Information has become infrastructure. Visibility has become currency. Observation has become routine. None of those developments automatically signal the decline of freedom, but neither should they pass without thoughtful examination. Free societies remain free not because they reject technology, but because they continue asking difficult questions long after the technology has become commonplace.

ConclusionSeveral months after I finished interviewing people for this article, I found myself waiting in line outside a neighborhood pharmacy. It was an entirely forgettable afternoon. Parents hurried children toward parked cars. Delivery drivers loaded packages into vans. A security officer greeted customers with polite indifference. Overhead, a traffic camera monitored the intersection while a small drone circled in the distance, assisting firefighters responding to an accident several blocks away. Nobody looked surprised. Nobody stopped to watch. Life simply continued.

Standing there, I realized that nothing in front of me would have seemed ordinary to someone transported from the late 1990s. Not because the scene was dramatic, but because it wasn't. The extraordinary had quietly become routine. Cameras no longer represented special occasions. Digital records no longer required deliberate effort. Armed security no longer implied immediate danger. Technology had woven itself so thoroughly into the background of daily existence that noticing it required conscious effort. Perhaps that is how every major societal transformation ultimately succeeds—not by demanding attention, but by becoming too familiar to attract it.

The purpose of recognizing these changes is not to romanticize the past or predict an inevitable dystopian future. Modern surveillance has solved crimes, rescued missing children, coordinated disaster response, protected critical infrastructure, and improved countless aspects of public safety. Those achievements deserve acknowledgment. At the same time, every generation inherits the responsibility to ask whether the systems it builds continue serving the public interest as they expand. Security and liberty have never been opposing absolutes. They are living principles requiring constant adjustment as societies evolve.

Preparedness, in its deepest sense, has never been about stockpiling equipment or anticipating catastrophe. It begins with observation—the willingness to notice slow-moving changes before they become permanent realities. The families most likely to navigate uncertain times successfully are often not the loudest or the most heavily equipped. They are the ones who remain curious, who adapt without surrendering their judgment, and who understand that resilience depends as much upon awareness as it does upon resources.

History rarely announces that it has entered a new chapter. More often, it whispers through ordinary days until one morning people look around and struggle to remember when the world became different. By then, the cameras have already been mounted, the drones have become background noise, the security checkpoints feel routine, and the debate is no longer about what is changing—but about whether anyone still remembers that it changed at all.

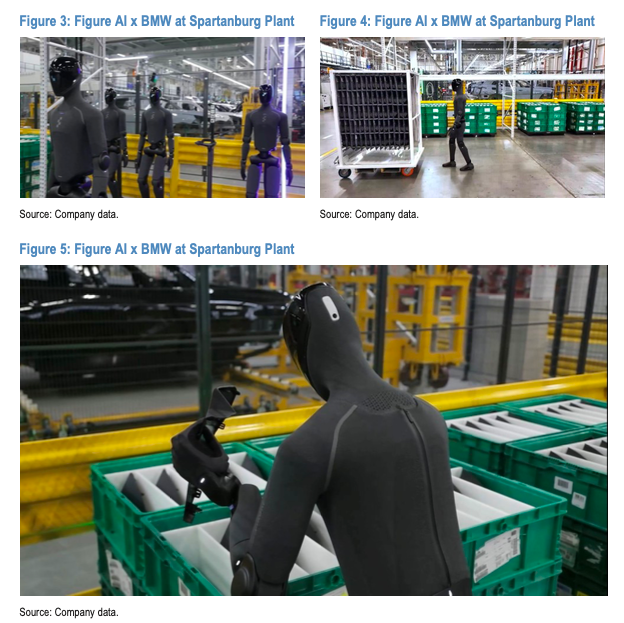

Tyler Durden Fri, 07/17/2026 - 23:25Japan plans to acquire 27,500 Nvidia Rubin chips as part of a $2.4 billion, government-backed push to develop domestic humanoid robotics models and reduce its dependence on foreign AI. This major effort comes as physical AI comes after data center buildouts, with global shipments of humanoid robots expected to surge next year.

Bloomberg reports that the newly formed Noetra Corp. will oversee the project and build an estimated 140-megawatt data center, scheduled to begin operating in about two years.

Sony, SoftBank, NEC, Fujitsu, and Toyota-backed Preferred Networks are among the top companies supporting the domestic AI push, which seeks to consolidate Japan's fragmented AI programs under one roof.

Noetra plans to release the first AI model tailored for industrial robots in Q1 2027. Japan is positioning itself to capture 30% of the expected $370 billion global robotics market by 2040.

Bloomberg quoted Nvidia CEO Jensen Huang as saying that Japan will require significantly more data centers, power infrastructure, and computing capacity to compete with the US and China, calling the Noetra project "just the beginning."

"We're going to be building a lot more infrastructure here," Jensen said. "This is just the beginning."

Physical AI is emerging rapidly across humanoid robotics, warehousing, autonomous trucking, construction, and even the home. These robots are being designed, tested, and, in some cases, deployed on factory floors.

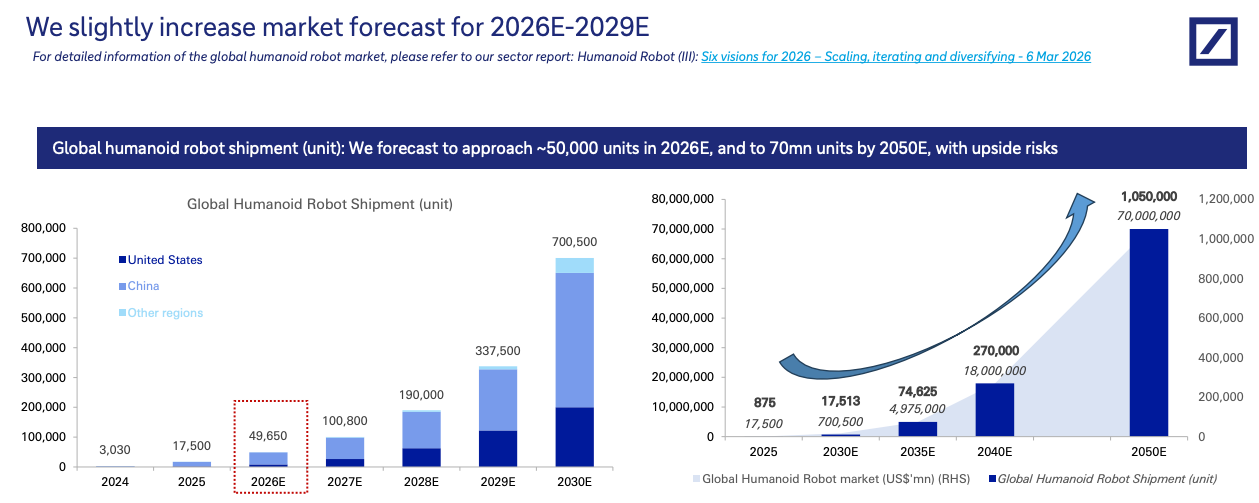

via Goldman Sachs

A recent Deutsche Bank report shows that global shipments are poised to surge.

Related:

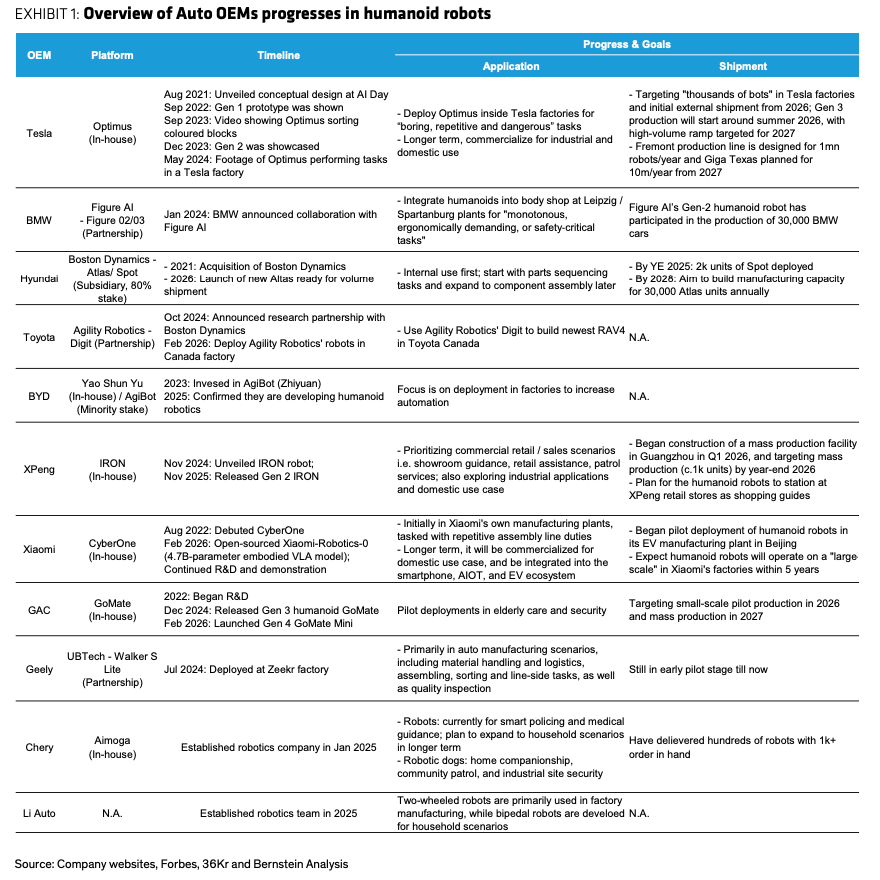

List of auto companies pursing humanoid robotics development:

We outlined what readers need to understand about this evolving space in a note titled "Current State Of Physical AI: Everything You Need To Know."

Tyler Durden Fri, 07/17/2026 - 23:00Authored by Jim Davis via AmericanThinker.com,

In a Zoom video call in 2023, a leader of the Democratic Socialists of America said, “Our goal is communism.” It was published as part of a compilation in April 2026.

None of the Democratic Socialists disavowed it. Nobody posted a “clarifying statement” distancing the DSA from that statement.

So that’s who they are. Their goal is communism.

The name of that leader is David Jenkins. He’s a member of the DSA’s National Political Committee, so he ought to know.

He told us who they are, so we should believe him.

Extreme leftist candidates (including DSA candidates) from past elections include

AOC, Rashida Tlaib, Ro Khanna, Ilhan Omar, and Pramila Jayapal.

Cory Booker, Ayanna Pressley, Bernie Sanders, and Cori Bush.

Extreme leftist DSA candidates who have popped up in the current cycle:

James Talarico in the Senate, who has embraced every nutball LGBTQ/trans theory on the planet, wrapped up in a sugary faux Christian coating.

Graham Platner was also running for Senate, after everyone knew about his Nazi tattoo, his active social media account at a site notorious for pedophiles chatting with little kids, and multiple credible allegations from conservative ex-girlfriends. Platner was finally taken down by another credible allegation, this time from a liberal ex.

In the House, a whole tribe of new candidates, including a sociology Ph.D. candidate who started a new “Death to America” campus club, a former associate of the “Blind Sheikh” who masterminded an early bombing attack on the World Trade Center (WTC), and people who think we deserved 9/11.

When people tell you who they are, believe them.

Their strategy is to primary more moderate Dems and take as many of the Democrats’ “safe seats” as possible. In such races, any actual competition is purely intramural, between Democrat factions. Republicans always lose these races in November, and sometimes they don’t even bother to run a candidate. The real battle is the Democrats’ primary.

Cori Bush is the only one from the initial DSA wave of 2016–2022 who “washed out,” by winning primaries for a few years, then losing one to a mainstream Dem. Clearly, she’s being candid about her DSA identity while she’s trying to get back into House of Representatives.

Recently, her campaign posted a group photo from a July 8 meeting of the St. Louis DSA chapter, showing her next to a communist “influencer” named Christopher Winston. He calls himself “BlackRedGuard” online and identifies as a Maoist.

This guy thinks landlords should be shot. He’s suggested he would “execute” a political rival.

From Daily Wire:

Winston can be seen standing next to Bush with a shirt reading “armed minorities.” ...

“I’m so proud to have DSA by my side, united in our fight against price gouging, big real estate, and billionaires influencing our politics,” [Bush] said. ...

During a stream in March 2024, Winston said that “we’re going to execute you after the revolution” in response to a video leftist activist Shaun King made discussing fraud accusations. Winston said that he hoped that cancer “eats” King’s “a**hole out” and called him an “albino snake.”

In other appearances, Winston argued that “burning a Waymo is not political violence” and argued that landlords should be greeted by “a strongly worded letter in the form of a very hot piece of metal.” ...

In other statements, Winston pledged to seize homes from landowners and argued that “the ultimate form of international solidarity is to make revolution in the United States.”

“Communists don’t want to take away your house. We’ll cancel your mortgage. You can have one house, not a dozen. Excess properties will be taken from landlords and distributed to actual families to live in,” he said in one recent post.

When they honestly tell you such things about themselves, believe them.

None of these people thinks America’s institutions have a right to exist in their present form. America’s institutions, they say, must be torn down and rebuilt into a more diverse socialist/DIE paradise. These are people who think the destruction of the WTC on 9/11 was not only well deserved, but necessary. And they think borders shouldn’t exist.

To illustrate this glorious revolutionary mindset, they’re whining about Elon Musk being the world's first trillionaire. But I don’t think they would have objected if Hunter Biden had been the world's first trillionaire. They have zero interest in cleaning up any of the fraud, greed, waste, graft, and corruption among Democrats.

None of these people thinks Israel has a right to exist at all. Every square inch of Israel, they say, belongs to the glorious and noble Palestinian people, represented by Hamas and Hezb’allah. And we found out on October 7, 2023 how that would end.

Cori Bush and other DSA luminaries haven’t distanced themselves from any of Winston’s statements, or challenged the authenticity of that Jenkins video clip. Their goal is communism.

We must be alert to the fact that political parties similar to the DSA have gained influence or taken control in such allied nations as the United Kingdom and Germany. We must take note of the fact that these are becoming the new sexual assault capitals of the world due to Muslim immigration.

In Australia, a left-wing party has taken charge. Law-abiding Australians are unarmed, which means the criminals are the only ones with guns, producing the Bondi Beach massacre.

We all need to recognize that the DSA and its overseas comrades are poisonous for America and our allies in the rest of the industrialized First World. They are toxic. And here in America, they must be limited to the tiny number of “safe Democrat” seats they’ll eventually have after November.

Tyler Durden Fri, 07/17/2026 - 22:35The Israeli government has stripped Nile crocodiles of their protected status, paving the way for a proposal to build a detention facility for Palestinians surrounded by the reptiles, Israeli media reported on Thursday.

Environment Minister Idit Silman signed a decree on Wednesday reclassifying Nile crocodiles as a "specially managed wild animal" - a new legal category that allows the state to keep the animals for security purposes, according to Israeli news site Ynet. In the decree, Silman said Israel's security forces could now keep crocodiles under specific conditions.

via Britannica

via Britannica

According to Ynet, the move went against the advice of the Environment Ministry's legal adviser and environmental groups. The decision follows months of pressure from National Security Minister Itamar Ben Gvir, who in December proposed building a prison encircled by crocodiles.

Ben Gvir, who oversees the Israel Prison Service (IPS), said he was inspired by Florida's controversial immigration detention centre, dubbed "Alligator Alcatraz".

Officials at the Israel Nature and Parks Authority had previously argued that crocodiles should only be kept for education and research. The Environment Ministry's legal adviser, Neta Drori, also opposed the plan, saying it lacked a sufficient legal and professional basis.

The IPS argued its staff could handle crocodiles because of their experience working with attack dogs, an argument Drori rejected. "The IPS does not appear to have expertise in raising dangerous wild animals such as crocodiles," she wrote, concluding that the legal requirements for the declaration had not been met.

Despite that opinion, Silman approved the measure this week.

Ben Gvir celebrated the decision on Facebook on Thursday, posting an AI-generated image of himself holding a crocodile on a lead. "Damn terrorist, thinking of trying to escape? Think again," the minister wrote.

Since what critics allege is genocide in Gaza began in October 2023, Ben Gvir has overseen a sharp deterioration in conditions for Palestinians held in Israeli prisons, including torture, starvation and degradation. Human rights organizations have accused Israel of widespread abuses and have described some detention facilities as "torture camps".

'Significant risks'Silman's decision drew opposition from the Israel Nature and Parks Authority (INPA) and environmental groups, which argued the move is unlawful and puts both crocodiles and the public at risk.

The INPA said there was "no sufficient professional basis" to permit crocodiles to be kept at security facilities. The agency, which is responsible for protecting Israel's wildlife, warned that introducing crocodiles into IPS facilities would create "significant risks", adding that it doubted the prison service could provide appropriate care for the animals.

In a joint statement, several environmental organizations said they "strongly object to the use of animals as a means of guarding and deterrence".

"Crocodiles are sentient beings, with complex needs for space, water, temperature and natural behavior," the groups said, arguing that prisons should rely on conventional security measures instead.

They also questioned the proposal's effectiveness, noting that crocodiles "slow down their metabolic rate, become very sluggish and stop eating" during winter.

Illustrative: would be something like this.

Illustrative: would be something like this.

"Security should be achieved through real means, not through animals," the statement concluded.

Nile crocodiles have been a protected species in Israel since 2013. Before then, crocodile farms operated as tourist attractions, but many switched to breeding the animals for their skins as visitor numbers declined.

Last year, the Israeli military killed more than 250 Nile crocodiles at a farm in an Israeli settlement in the occupied West Bank, prompting condemnation from animal welfare groups, which accused it of slaughtering protected animals.

Tyler Durden Fri, 07/17/2026 - 21:45Moscow and Pyongyang have quite obviously deepened their relations in unprecedented ways over the past years since the Ukraine war began, and this has been most on display with the transfer of thousands of North Korean troops in support of Russian forces, and DPRK soldiers even losing their lives while fighting Ukraine.

So it's only to be expected that Russia side with North Korea in the long-running conflict and standoff with South Korea. But now the Kremlin senses Seoul is moving ever closer to NATO, to the point that it's calling out the deepened military relations.

Russia has newly made clear its position that it is unacceptable for South Korea to become a de facto participant in the alliance’s rearmament efforts.

The Russian Foreign Ministry said in a new statement issued following a meeting between Deputy Foreign Minister Andrey Rudenko and South Korean Ambassador to Moscow Lee Seok Bae:

"The Russian side expressed serious concern over Seoul’s growing drift toward NATO, as demonstrated, among other things, by the Republic of Korea’s practical steps to deepen military and military-technical cooperation with the North Atlantic Alliance, the consequences of which pose a threat to Russia’s security," the statement said.

The ministry stated that "it is unacceptable for the Republic of Korea to become a de facto participant in NATO's qualitative and quantitative rearmament process, as the alliance has openly declared its preparations for war with Russia."

Of course, South Korea is not a NATO member and full membership remains unrealistic; however, it is seen by Brussels as a highly integrated "Indo-Pacific partner" - and of course the United States has a permanent large-scale troop presence there.

Major General Eray Üngüder, Director of NATO’s Cooperative Security Division, declared in June that "The Republic of Korea is a longstanding Partner of NATO and we are grateful to have this strongly committed partnership."

And NATO describes on its website of relations with Seoul that "This collaboration, initiated in 2005, involves joint efforts in several fields including cybersecurity, capability development, new technologies and countering hybrid threats. This year’s conversations primarily addressed topics like interoperability, standardization and cyber exercises."

But Moscow definitely sees thing differently. It agrees with Kim Jong Un that Washington is an 'imperialist' power and hegemon, and through constant military flexing, sows instability from Eastern Europe to the South Pacific.

Tyler Durden Fri, 07/17/2026 - 21:20Authored by David Manney via PJMedia.com,

Fake training records can move an unprepared driver one step closer to a commercial license.

Transportation Secretary Sean Duffy and Homeland Security Secretary Markwayne Mullin are now investigating about 75 entry-level driver training schools suspected of doing exactly that.

Federal Motor Carrier Safety Administration (FMCSA) has identified approximately 75 entry-level driving training schools suspected of fraudulent activities, including using improper driver certifications, falsifying training records, and failing to properly train drivers applying for CDLs, among other violations. USDOT will engage DHS’s Homeland Security Investigations (HSI) in its investigations of these schools.

“USDOT has spent the last year rooting out bad actors from our trucking industry,” said U.S. Transportation Secretary Sean P. Duffy. “We've knocked over 24,000 drivers off our roads for failing to speak English, forced states to cancel over 28,000 licenses illegally issued to foreign drivers, and purged over 9,500 unqualified training schools from our FMCSA registry. DHS will be a force multiplier of our efforts to clean up America's roads. President Trump is using every lever at his disposal to ensure the safety of American families.”

“Too many American lives have been lost in completely avoidable accidents because illegal aliens have been granted commercial driver’s licenses to drive trucks and 18-wheelers on America’s roadways,” said DHS Secretary Markwayne Mullin. “DHS law enforcement is partnering with the Department of Transportation to eliminate CDL fraud, strengthen the integrity of the CDL system, and investigate commercial driver’s license schools throughout the country. This is a whole of government approach, to keep America’s roads safe.”

This is part of the administration's ongoing efforts to root out fraud from American trucking and restore integrity to the industry.

Federal officials say the schools may have used improper certifications, falsified training records, or failed to train CDL applicants properly. Homeland Security Investigations will work with the Federal Motor Carrier Safety Administration to determine whether poor instruction crossed into criminal fraud.

The licensing system gives training schools enormous power. Federal rules require many first-time applicants to complete approved instruction before taking a CDL skills test.

Registered schools then submit completion records electronically, and state licensing agencies use those records to decide whether an applicant may test.

Providers also self-certify that they meet federal standards when joining the registry. A dishonest school damages the first major checkpoint before an applicant ever sits for the road test. Fraud at that stage reaches far beyond paperwork.

Duffy's department had already found deep problems. In February, more than 300 investigators conducted 1,426 on-site inspections across all 50 states. They issued 448 proposed removal notices, while 109 providers removed themselves after learning investigators were coming. Another 97 remained under investigation.

The violations were not harmless technical errors. Investigators found instructors without the proper licenses, schools using the wrong vehicles, incomplete student assessments, and providers that failed to meet their state requirements. One school had even trained bus drivers.

Nearly 10,000 training locations have now been removed from the federal registry. The department also says more than 24,000 drivers were taken out of service for failing English proficiency requirements, while states canceled more than 28,000 licenses illegally issued to foreign drivers.

Those numbers expose a system that went too long without firm inspection. The new joint probe adds criminal investigators who can follow records, payments, identities, and possible coordination between schools and applicants.

Legitimate driving schools and qualified immigrant drivers should welcome the cleanup. Fraudulent operators cheapen the work of every instructor who teaches the rules and every driver who earns a CDL lawfully. They also leave responsible trucking companies exposed when a bad credential slips through.

A commercial license is permission to operate some of the largest vehicles on American roads. Families traveling beside them can't inspect a driver's school records or verify who provided the training. The government carries that duty before the license is issued.

Duffy and Mullin are finally treating driver training as part of highway safety rather than an administrative formality. The 75 schools remain under investigation, and officials still must establish what each one did. Every false record should be traced to the driver, licensing office, and person who profited from it because a forged certificate should never become a license to endanger everyone else.

Tyler Durden Fri, 07/17/2026 - 20:55While the Pentagon publicly clings to a $30 billion price tag for its war against Iran, internal Defense Department assessments (unsurprisingly) paint a far more staggering picture: the true cost is rapidly closing in on the $80 billion to $100 billion range, according to NBC News.

The Pentagon's Office of Management and Budget told Congress on June 30 that US military operations against Iran so far is $30 billion: "We’ve spent about $30 billion," OMB Director Russel Vought told the House Appropriations Committee.

NBC's new assessment bluntly states the following, however: "The cost of the war with Iran could be more than triple the most recent estimate of roughly $30 billion, according to three U.S. officials and three people familiar with the internal cost estimates."

The lower figure was reportedly initially floated based a classic Washington accounting trick which only evaluates the cost of expended missiles and munitions while conveniently ignoring the charred remnants of American hardware and damaged bases littering the Gulf states after Iranian retaliatory attacks, the report explains.

The estimate featured in the NBC report accounts for actually rebuilding those installations previously attacked by Iran. Judging by how things are going this week - after five consecutive days of renewed fighting - the final bill from damage will only keep pushing up from here.

It has been well documented that while American troops at Gulf bases across the Strait of Hormuz and Persian Gulf were by and large pulled back from near 'front lines' - large US military assets like refueling tankers were in some cases left behind, resulting in scenes like the following:

The Telegraph: In a picture verified by AFP, the mangled airframe of the US air force jet stands on the runway of Prince Sultan air base in Saudi Arabia.

The Telegraph: In a picture verified by AFP, the mangled airframe of the US air force jet stands on the runway of Prince Sultan air base in Saudi Arabia.

"Five U.S. Air Force refueling planes were struck and damaged on the ground at Prince Sultan air base in Saudi Arabia, according to two U.S. officials," The Wall Street Journal reported in mid-March. Each one costs hundreds of millions.

"The tankers were hit during an Iranian missile strike on the Saudi base in recent days, the officials said," WSJ detailed at the time. "U.S. Central Command declined to comment. The tankers were damaged but not fully destroyed and are being repaired, one of the officials said. No one was killed in the strikes."

And in Bahrain, home of the US Navy's Fifth Fleet, damage to military facilities is already estimated at $1 billion. Heavily fortified installations in Kuwait have also taken a severe beating, with both these tiny Arab Gulf states being favored targets of IRGC projectiles of late.

In the meantime, with a $1.5 trillion budget battle looming this autumn, the Pentagon is currently urging Congress to approve $68 billion supplemental funding package just to keep the lights on, but as the Iran war drags on with few clear objectives outlining an endgame, defense officials are hitting a wall of bipartisan skepticism among lawmakers.

One D.C. watchdog group, Public Citizen, has stated this week: "The American people are fed up with spending more on bombs and less on basic needs. And they are furious with a pointless, deadly, illegal, unconstitutional and protracted war that is costing lives and driving up gas prices."

Tyler Durden Fri, 07/17/2026 - 20:30Authored by William Brooks via The Epoch Times,

Secretary of State Marco Rubio’s recent announcement of a “whole-of-government” campaign to challenge the International Criminal Court (ICC) has generated predictable discourse worldwide.

The Trump administration is applying diplomatic pressure on allied governments to reconsider their support for the Court. Washington is calling for expanded sanctions against ICC officials, visa restrictions, and renewed insistence that the Court has no lawful authority over citizens of sovereign nations.

For the usual globalist critics, this is just another example of Trumpian unilateralism. But for sensible Americans, it reflects the president’s determination to place “America First” ahead of international institutions.

In fact, the issue deserves thoughtful examination that goes beyond ideological rhetoric. At its heart lies one of the oldest questions in constitutional government: Who has the ultimate authority to judge the citizens of a sovereign nation—its own national institutions, or an international tribunal whose judges are beyond the reach of that nation’s electorate?

The answer explains why every American administration since the ICC’s creation has refused to recognize the Court’s jurisdiction over American servicemen and government officials.

The International Criminal Court was established under the Rome Statute in 1998 and formally began operations in 2002. It was created with an admirable purpose: to prosecute individuals responsible for genocide, crimes against humanity, war crimes, and, more recently, the crime of aggression when national courts either cannot or will not act.

The horrors of Rwanda and the former Yugoslavia convinced many that the “international order” needed a permanent institution capable of bringing the world’s worst criminals to justice. Few people disputed that objective.

Since World War II, the United States has played a significant role in shaping modern international criminal law. From the Nuremberg trials to the creation of temporary tribunals for Yugoslavia and Rwanda, successive American governments have supported the prosecution of genuine war criminals.

What Washington has never accepted is the proposition that an international court may exercise criminal jurisdiction over American citizens without the United States’ consent.

Global OverreachBill Clinton authorized the signing of the Rome Statute during the final days of his administration, but he deliberately declined to submit it to the Senate for ratification, acknowledging significant constitutional concerns.