12 Glaring Realities Of Marxist Socialism

Authored by Christian Milord via The Epoch Times,

In a free society that embraces free markets and the rule of law, young people must be made aware of the glaring realities regarding the alleged “fuzzy and warm” nature of Marxist (collectivism, communism, progressivism, socialism) iterations.

There are at least twelve aspects of the Marxist ideology that are clear and present dangers to democratic nations as well as undemocratic countries.

First, Marxism was founded on the stark concept of atheism. Consequently, it attempts to dismantle the Judeo-Christian faith that has been an anchor of civilization for thousands of years and helps people to navigate life’s challenges. Marxists also oppose the traditional family, which is the building block of any culture and bolsters societal bonds. On every life category, intact families are far more successful than broken families.

Next, Marxist policies encourage folks to be intellectually and physically lazy as they rely on bureaucratic government for all of their needs. This reliance generates an unearned entitlement mentality that expects others to supply the needs of those who refuse to accept personal responsibility. Minimal effort is applied to studying and working, yet the “entitled” expect to earn high salaries regardless of the effort they put forth.

Third, Marxists are quite generous with the money confiscated from job creators, but they are stingy with their own money. However, most of the money and possessions that are seized by Marxist leaders end up with their cronies and are not redistributed to the lower-income workers they claim to be helping. The hypocrisy is staggering.

Fourth, Marxist influencers compete with one another to see who the best liar is as they deceive the vulnerable who might believe promises that are too good to be true. Marxists use deception as a means to control the masses and keep them on their heels. They talk a good game about socialism as a paradise on earth yet do everything they can to turn that alleged nirvana into a hell on earth.

Fifth, Marxism is an arbitrary system built on a foundation of contradictions. It can hand out some goodies but just as easily withdraw them. Marxists believe that they can alter laws whenever they feel the urge, thus using raw power plays to confuse and divide people, and consolidate power in the hands of a few. Arbitrary laws can hinder people from advancing economically and can also create insecurity.

Sixth, for an ideology that claims it will usher in equality, Marxism certainly is fixated on economic class, color, gender, and race. Apparently, some are more equal than others. Instead of equal opportunity, Marxists favor the equity of prearranged outcomes. Many Marxist spokespersons are often educated academics who pretend victimhood and fear competition in the real world yet believe they are smarter than everyone else. They’ve learned nothing about good citizenship and wisdom, while displaying a common sense deficit. Marxists envy folks who keep their noses to the grindstone, and lash out at those who possess discipline, deferred gratification, and a healthy work ethic.

Seventh, Marxists promise freedom and security to those who will join their cause, yet wealth is stolen from others, and security only exists for those at the top of the pyramid. In other words, everyone is equally miserable under Marxism except for the jackbooted leaders who profit from the spoils acquired from their “legalized” theft. For proof, just examine the misery index of folks in China PRC, Cuba, Iran, N. Korea, and Russia.

Eighth, it’s puzzling why Marxists who reside in free societies lack the courage to move to the autocratic societies they admire. Is it because they don’t even believe the mantras they keep repeating, or do they want to have their cake and eat it, too? They denounce the blessings of free enterprise and liberty at the same time as they partake of them. Unfortunately, they have taken their blessings for granted. Do they really want to transform America into a dysfunctional nation that has constant shortages of goods and services?

Ninth, Marxism promotes the darker facets of human nature rather than its nobler strivings. Marxists turn lies into the truth and truth into lies. They oppose the arts, constructive creativity, and innovation and constantly push monolithic groupthink instead of critical thinking. In other words, Marxism is extremely boring and lacks a sense of humor.

Tenth, Marxists never learn from history and thus are doomed to repeat it, even after the carnage that’s been generated by their dystopian policies for over a century. Someone once noted that doing the same thing over and over and expecting different results is the definition of insanity. That’s the Marxist playbook in a nutshell.

Eleventh, Marxists glorify the vices and demonize traditional virtues even while they carry out plenty of virtue signaling. They condescendingly lecture us about upholding democracy and liberty at the same time as they attempt to erode economic freedom, educational freedom, and individual freedom.

Finally, Marxism is highly immature. Marxists rarely learn from the past and thus triple down on failure. They blame others for their own fascist behavior, which is an example of denial and projection. They demand to get what other folks have earned, which is childish and immoral. Marxists side with totalitarian entities and mob rule, while opposing the sole Middle East democracy, Israel. Most Marxists only embrace law enforcement when it is provided to protect unlawful immigrants and themselves, and when it is used to punish law-abiding folks.

This is why it is imperative to vigorously oppose Marxism by all means necessary.

Tyler Durden Mon, 08/03/2026 - 23:25

via Reuters

via Reuters President Donald Trump prepares to board Air Force One at Morristown Municipal Airport in Morristown, N.J., on Aug. 2, 2026. Anna Moneymaker/Getty Images

President Donald Trump prepares to board Air Force One at Morristown Municipal Airport in Morristown, N.J., on Aug. 2, 2026. Anna Moneymaker/Getty Images

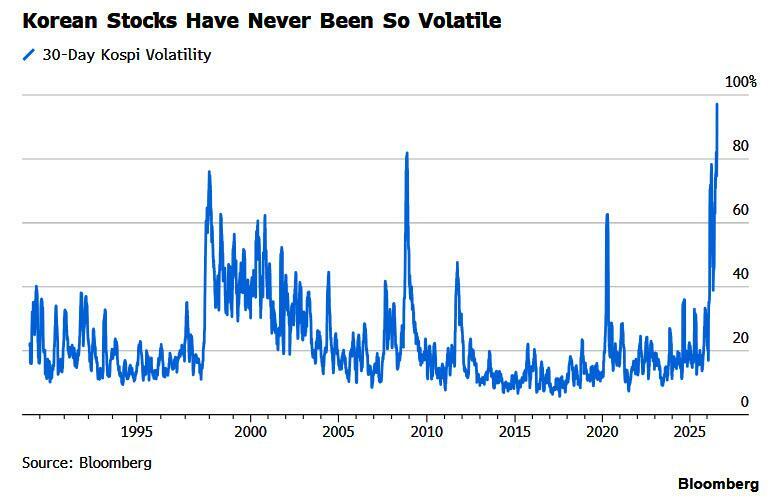

Near the main gate of the National Assembly in Yeouido, Seoul, there are condolence flowers installed calling for the delisting of single-stock leveraged ETFs. (Photo: Yonhap News)

Near the main gate of the National Assembly in Yeouido, Seoul, there are condolence flowers installed calling for the delisting of single-stock leveraged ETFs. (Photo: Yonhap News)

South Korean President Lee Jae Myung attends an agreement-signing event at Villa Doria Pamphili in Rome, Italy, June 12, 2026. REUTERS/Remo Casilli/File Photo

South Korean President Lee Jae Myung attends an agreement-signing event at Villa Doria Pamphili in Rome, Italy, June 12, 2026. REUTERS/Remo Casilli/File Photo

Illustration by The Epoch Times, Zereshk/CC BY-SA 3.0

Illustration by The Epoch Times, Zereshk/CC BY-SA 3.0 The Department of Justice in Washington on Feb. 21, 2026. In May and June, the Justice Department, along with the attorneys general of Texas and Ohio, secured settlements with large hospitals over allegations of fraudulent insurance billing practices related to “gender-affirming care” for children. Madalina Kilroy/The Epoch Times

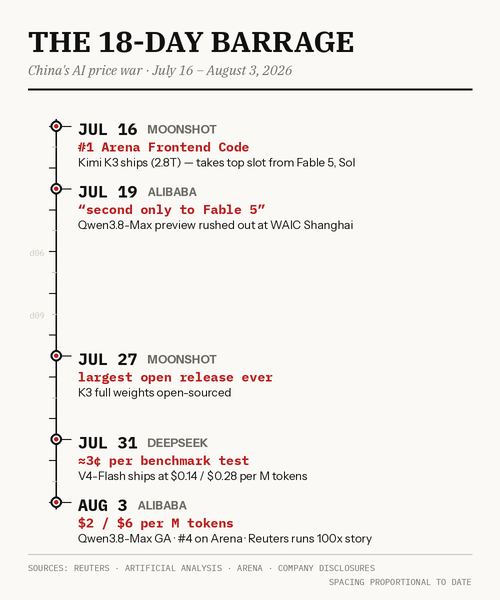

The Department of Justice in Washington on Feb. 21, 2026. In May and June, the Justice Department, along with the attorneys general of Texas and Ohio, secured settlements with large hospitals over allegations of fraudulent insurance billing practices related to “gender-affirming care” for children. Madalina Kilroy/The Epoch Times Sarah Rogers / MITTR | Photo Getty

Sarah Rogers / MITTR | Photo Getty

A large banner is seen at a campaign event for a proposed "billionaire tax" in Los Angeles on Feb. 18, 2026. | Jae C. Hong/AP

A large banner is seen at a campaign event for a proposed "billionaire tax" in Los Angeles on Feb. 18, 2026. | Jae C. Hong/AP

Dr. Anthony Fauci, former director of the National Institute of Allergy and Infectious Diseases at the National Institutes of Health, testifies before the Senate Committee on Homeland Security and Governmental Affairs in Washington on July 29, 2026. Madalina Kilroy/The Epoch Times

Dr. Anthony Fauci, former director of the National Institute of Allergy and Infectious Diseases at the National Institutes of Health, testifies before the Senate Committee on Homeland Security and Governmental Affairs in Washington on July 29, 2026. Madalina Kilroy/The Epoch Times

via Reuters

via Reuters

Recent comments