Key Events This Week: Core PCE, Global PMIs, Micron Earnings And Fed Talk

The main data highlights this week are the global flash PMIs tomorrow, and the US core PCE on Thursday. Elsewhere, other data of interest include the Ifo survey in Germany (Wednesday), Tokyo CPI in Japan (Friday), and CPI reports in Canada (today) and Australia (Wednesday). Also focus will be on the UK where Keir Starmer announced his resignation earlier today and attention will turn on succession planning.

After a hawkish FOMC last week with a clear shift in style from new Fed Chair Kevin Warsh, DB economists now have two 25bps hikes in their Fed forecast while Bank of America raised their forecast and now expect 3 hikes in 2026, reversing its prior no-change forecast on strong data and a hawkish Fed under Chair Warsh. DB warns that the US economy needed tighter policy but were waiting for the meeting to confirm the tightening view. The central scenario sees two rate increases this year, likely in September and December, taking the fed funds rate to around 4.1%, followed by a prolonged pause through 2027. Easing is then expected to resume in the first half of 2028, with around 50 basis points of cuts, potentially delivered in March and June, bringing policy back towards a neutral range of roughly 3.5–3.75%.

In terms of the US week ahead, DB economists expect appearances by Williams and Goolsbee on Thursday to be particularly informative. Williams, who also serves as Vice Chair of the FOMC, is seen as one of those not currently predicting a hike this year, while Goolsbee is viewed as leaning towards around 50 basis points of tightening.

Earlier that day, attention will center on the data flow. Economists expect May personal income to rise by around 0.4% (from flat previously) and consumption to increase by 0.6% (from 0.5%). The core PCE deflator is projected to rise by around 0.37% month-on-month, up from 0.24%. On this basis, the year-on-year rate would move higher to approximately 3.44%, marking the strongest reading since October 2023 and reinforcing the narrative of persistent underlying inflation. The Fed will also release its bank stress test results on Wednesday and there is other second tier data you can see in the day-by-day calendar at the end as usual.

Over in Europe, in addition to the PMIs, sentiment indicators in Germany will include the Ifo survey (Wednesday) and the July GfK consumer confidence print (Thursday). In France, there will be business confidence tomorrow and consumer confidence on Thursday. Finally, the ECB will release its May consumer expectations survey on Friday, with inflation expectations in focus. ECB speakers will include President Lagarde amongst others.

In Asia, inflation prints due include the Tokyo CPI for June on Friday in Japan and Australia’s May CPI due Wednesday. Other notable data features BoJ’s Summary of Opinions from its June meeting (Wednesday), Australia’s labour force survey (Thursday) and the 1-year and 5-year loan prime rates in China (Monday).

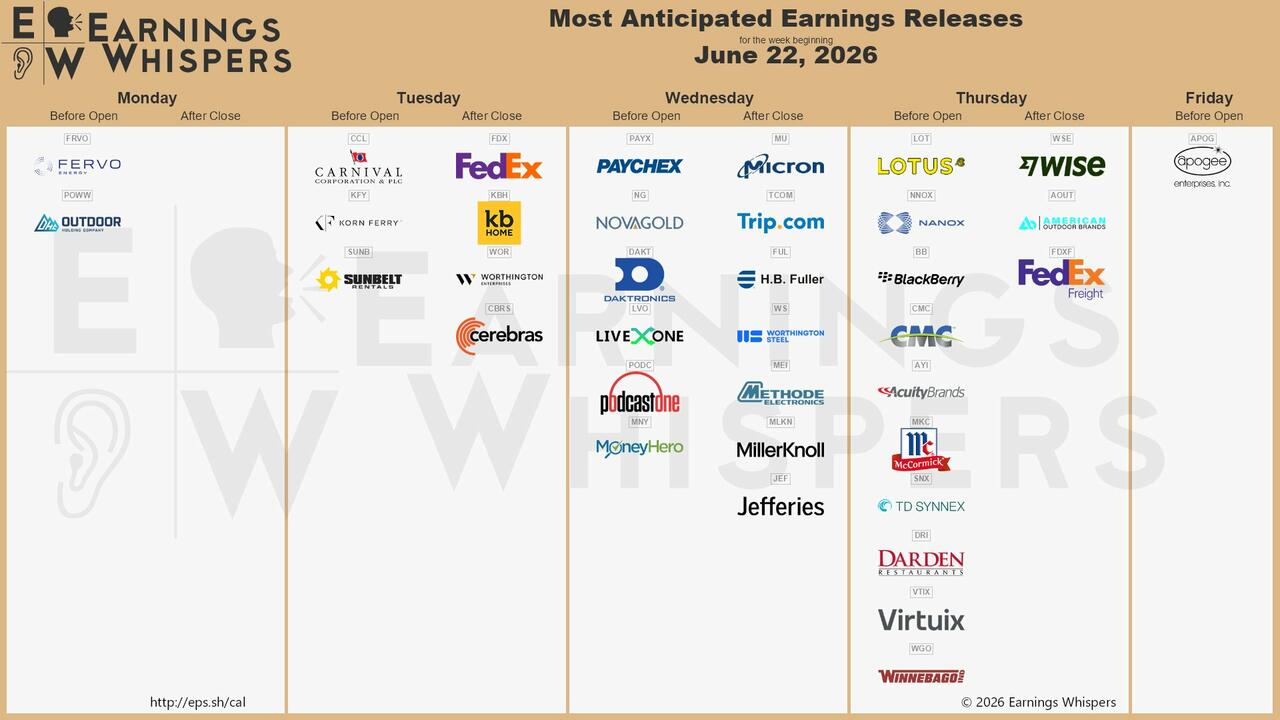

Finally, there will be a few notable earnings reports out next week, including FedEx, Cerebras and Carnival tomorrow as well as Micron and Jefferies on Wednesday. Micron is up around 830% over the last year and around 250% since the end of March with a market cap of nearly $1.3tn. So it’s becoming one to follow from the macro side.

Courtesy of DB, here is a day-by-day calendar of events

Monday June 22

- Data: Eurozone June consumer confidence, Canada May CPI, China 1-yr and 5-yr loan prime rates

- Central banks: Fed's Waller speaks, ECB's Lagarde and Kocher speak

Tuesday June 23

- Data: US, UK, Japan, Eurozone, Germany and France June flash PMIs, US June Philadelphia Fed non-manufacturing activity, Richmond Fed manufacturing index, business conditions, France June business confidence, May retail sales, EU27 May new car registrations

- Central banks: ECB's Lane and Vujcic speak, BoE’s Taylor and Dhingra speak

- Earnings: FedEx, Cerebras, Carnival

- Auctions: US 2-yr Notes ($69bn)

Wednesday June 24

- Data: US May new home sales, Q1 current account balance, Japan May PPI services, Germany June Ifo survey, Australia May CPI

- Central banks: ECB's Nagel and Cipollone speak, BoJ's Himino speaks, BoJ summary of opinions (June MPM), BoE’s Breeden and Dhingra speak, BoC summary of deliberations

- Earnings: Micron, Jefferies

- Auctions: US 2-yr FRN (reopening, $28bn), 5-yr Notes ($70bn)

- Other: Fed releases bank stress test results

Thursday June 25

- Data: US May PCE, personal income and spending, durable goods orders, Chicago Fed national activity index, June Kansas City Fed manufacturing activity, initial jobless claims, Germany July GfK consumer confidence, France June consumer confidence, Italy April industrial sales, Australia May labour force survey

- Central banks: Fed's Williams and Goolsbee speak, ECB's Moulin, Lane and Cipollone speak, BoJ's Tamura speaks, ECB Economic Bulletin

- Auctions: US 7-yr Notes ($44bn)

Friday June 26

- Data: US May advance goods trade balance, retail inventories, wholesale inventories, June Kansas City Fed services activity, JapanJune Tokyo CPI, Italy June consumer confidence index, economic sentiment, manufacturing confidence, ECB May consumer expectations survey

- Central banks: Fed's Kashkari speaks, ECB's Nagel and Vujcic speak

Turning just to the US, Goldman writes that the key economic data release this week is the PCE inflation report on Thursday. There are several speaking engagements with Fed officials this week, including events with Governor Waller and Presidents Williams, Goolsbee, and Kashkari.

Monday, June 22

- There are no major data releases scheduled.

- 09:00 AM Fed Governor Waller speaks: Fed Governor Christopher Waller will deliver opening remarks at the fifth conference on the International Roles of the US Dollar in Washington, DC. Speech text is expected. On May 22, Waller said that he is “prepared to be patient in holding policy at its current restrictive setting as we watch how the conflict evolves and what impact there is on inflation and inflation expectations.” He also noted that “if inflation expectations become unanchored, [he] would not hesitate to support an increase in the target range for the federal funds rate, but at this point that action is premature.”

Tuesday, June 23

- 09:45 AM S&P Global US manufacturing index, June preliminary (consensus 54.6, last 55.1): S&P Global US services index, June preliminary (consensus 51.0, last 50.7)

Wednesday, June 24

- 10:00 AM New home sales, May (GS +3.6%, consensus +3.2%, last -6.2%)

Thursday, June 25

- 08:30 AM Personal income, May (GS +0.5%, consensus +0.4%, last flat); Personal spending, May (GS +0.7%, consensus +0.5%, last +0.5%); Core PCE price index, May (GS +0.31%, consensus +0.3%, last +0.2%); Core PCE price index (YoY), May (GS +3.38%, consensus +3.4%, last +3.3%); PCE price index, May (GS +0.45%, consensus +0.5%, last +0.4%); PCE price index (YoY), May (GS +4.04%, consensus +4.1%, last +3.8%): We estimate that personal income and spending increased by 0.5% and 0.7%, respectively, in May. We estimate that the core PCE price index rose 0.31% in May, corresponding to a year-over-year rate of +3.38%. Additionally, we expect that the headline PCE price index increased 0.45% in May, or increased 4.04% from a year earlier.

- 08:30 AM Initial jobless claims, week ended June 20 (GS 230k, consensus 225k, last 226k); Continuing jobless claims, week ended June 13 (consensus 1,805k, last 1,810k)

- 08:30 AM Durable goods orders, May preliminary (GS -3.0%, consensus -5.0%, last +8.0%); Durable goods orders ex-transportation, May preliminary (GS +0.1%, consensus +0.6%, last +1.1%); Core capital goods orders, May preliminary (GS +0.3%, consensus +0.6%, last -1.0%); Core capital goods shipments, May preliminary (GS +0.3%, consensus +0.5%, last +0.4%): We estimate that durable goods orders declined 3% in the preliminary May report (month-over-month, seasonally adjusted) based on our tracking of commercial aircraft orders. We forecast a 0.3% increase in core capital goods orders—reflecting the increase in the new orders components in manufacturing surveys in May—and a 0.3% increase in core capital goods shipments—reflecting the continued increase in core capital goods orders in recent months.

- 08:30 AM GDP, Q1 third release (GS +1.6%, consensus +1.6%, last +1.6%); Personal consumption, Q1 third release (GS +1.4%, consensus +1.4%, last +1.4%): We estimate no revision on net to Q1 GDP growth at +1.6% (quarter-over-quarter annualized). We expect unrevised consumer spending growth at +1.4%.

- 03:40 PM New York Fed President Williams (FOMC voter) speaks: New York Fed President John Williams will give keynote remarks at the Crane Money Fund Symposium in New York City, NY. Speech text and Q&A are expected. On June 3, Williams said, “Monetary policy is exactly in the right place.” He also noted that he does not see “any need to raise or lower interest rates right now.”

- 06:30 PM Chicago Fed President Goolsbee (FOMC non-voter) speaks: Chicago Fed President Austan Goolsbee will discuss the forces shaping monetary policy and what they mean for the American economy at the Chicago Council on Global Affairs. Q&A is expected. On May 18, Goolsbee raised concerns about inflation and said, “We were making progress [on inflation], then we stalled, and now [the inflation problem] is getting worse.” On the labor market, he said, “The labor market might not be good, but it has been stable.”

Friday, June 26

- 08:30 AM Advanced goods trade balance, May (GS -$84.0bn, consensus -$85.0bn, last -$83.0bn); We estimate that the goods trade deficit widened slightly from $83.0bn in April to $84.0bn, reflecting a $16bn decline in gold exports that was largely offset by an increase in exports of energy goods.

- 10:00 AM University of Michigan consumer sentiment, June final (GS 49.5, consensus 50.0, last 48.9); University of Michigan 5-10-year inflation expectations, June final (GS 3.3%, last 3.4%)

- 11:30 AM Minneapolis Fed President Kashkari (FOMC voter) speaks; Minneapolis Fed President Neel Kashkari will participate in a panel at the Aspen Ideas Festival. On May 29, Kashkari said, “I think it is premature to conclude we need to be raising rates right away.” He also noted, “We need to keep watching the data and watching how the conflict in the Middle East unfolds before we want to make any adjustment.”

Source: DB, Goldman

Tyler Durden Mon, 06/22/2026 - 10:15

Ukrainian naval image of Turkish vessel up in flames.

Ukrainian naval image of Turkish vessel up in flames.

Roman bathhouse complex.

Roman bathhouse complex. Roman bone hairpins found in Nijmegen. Credit: Municipality of Nijmegen / BAAC / RAAP

Roman bone hairpins found in Nijmegen. Credit: Municipality of Nijmegen / BAAC / RAAP Reuters/BBC: "Cars queue at a petrol station on the peninsula in early June amid already restricted fuel sales."

Reuters/BBC: "Cars queue at a petrol station on the peninsula in early June amid already restricted fuel sales."

Michael Boes, Steak 'n Shake's chief Make America Healthy Again (MAHA) officer, in Irving, Texas, on June 15, 2026. Bobby Sanchez/The Epoch Times

Michael Boes, Steak 'n Shake's chief Make America Healthy Again (MAHA) officer, in Irving, Texas, on June 15, 2026. Bobby Sanchez/The Epoch Times A Steak 'n Shake restaurant in Middletown, Del., on July 26, 2019. The fast food chain in April hired a chief MAHA officer, an industry first. Jim Watson/AFP/Getty Images

A Steak 'n Shake restaurant in Middletown, Del., on July 26, 2019. The fast food chain in April hired a chief MAHA officer, an industry first. Jim Watson/AFP/Getty Images

Recent comments