Futures Rebound From "Chip-Wreck" Ahead Of Critical Micron Earnings

US stocks are set for a rebound with equity futures higher as Semis and Tech stage a partial recovery from yesterday’s "Chip-Wreck" as KOSPI retraced about 20% of its losses ahead of earnings from the single-biggest contributor to US outperformance this year: Micron’s third-quarter numbers are an even bigger deal than usual, following Tuesday’s shakeout of an overcrowded AI trade that’s has been priced for perfection. As of 8:00am ET, S&P 500 futures are 0.3% higher with Nasdaq 100 contracts up 0.5%. In premarket trading, equities are boosted by a bid for Semis (MU +3.6% with earnings tonight) with most of Mag7 higher. Within Cyclicals, Discretionary and Industrials are the standouts as Energy / Fins are mostly lower. Cyclicals poised to lead Defensives with Momentum factor flat. Bond yields are lower 1-2bp as the yield curve flattens, pushing 10Y yields ; USD remains bid even as real yields decline. DXY set a new 52-wk high today. Cmdty remain under pressure dragged by the Energy complex and weakness in Metals. Today’s macro data focus is on Home Sales ahead of tomorrow's update on GDP, PCE, Personal Income / Spending, Cap / Durable Goods, and weekly Claims.

In premarket trading, Alphabet (GOOGL) is up 0.5% after news the Google parent will replace Verizon in the Dow Jones Industrial Average. Verizon (VZ) is down 0.5%. Other Mag 7 stocks are mostly higher (Nvidia +0.6%, Tesla +0.6%, Meta +0.1%, Apple +0.6%, Microsoft -0.5%, Amazon -0.2%)

- Cerebras Systems (CBRS) falls 14% premarket after the newly public chipmaker gave an annual sales forecast that disappointed investors looking for it to take a bigger slice of the AI data center market.

- FedEx (FDX) is down 7% after the parcel delivery company posted its first earnings report since completing the spin off of its freight unit earlier this month. Results seem to have fallen short of investor expectations after a strong run-up in the first half of the year: the company cited margin pressure and global trade uncertainty in its outlook.

- FuelCell Energy (FCEL) rises 16% after the company said it reached an agreement with Fit Energy to supply 380 megawatts of clean on-site power for data centers using FuelCell Energy’s technology.

- Hertz (HTZ) slumps 16% after providing an update. The company also filed to offer $100m of stock.

- Twilio Inc. (TWLO) rises 3% as Goldman Sachs rates the software company buy with a Street-high $300 price target, citing AI tailwinds.

- Wendy’s (WEN) rises 23% as the stock climbed the ranks in Stocktwits and Reddit’s widely followed wallstreetbets forum.

In other company news, Qualcomm is hosting a highly anticipated investor day in New York. CEO Cristiano Amon and executives are using the event to outline the company’s next phase of growth and diversification strategy. And Nike is hiring David Denton as its next CFO, who is poised to leave Pfizer in August. SpaceX shares are fluctuating, after it sold $25 billion of investment-grade bonds.

While yesterday’s market action was wild for some chip stocks, there was no sense of over-reaction or panic across the market, according to Goldman traders. They said that on a 1 to 10 scale of overall activity level on their trading floor, the session was a 5, despite broad selling by long only and hedge funds. They also say that top-of-book liquidity remains shallow, exacerbating price action.

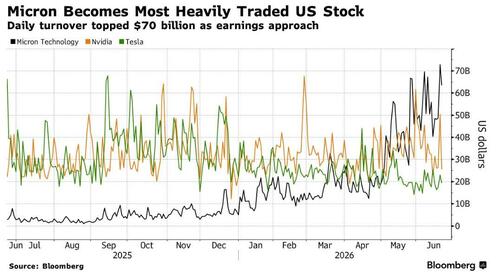

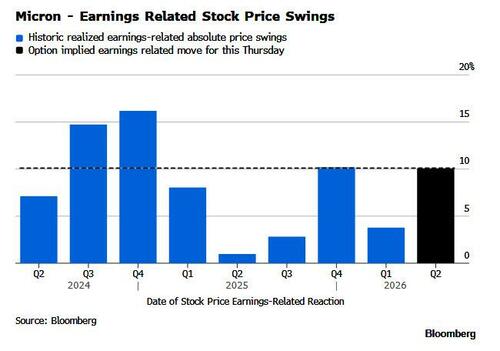

The recent swings are sharpening the focus on Micron, one of the biggest beneficiaries of roaring demand for chipmakers that stand to gain from the billions of dollars being plowed into AI infrastructure. The stock is up more than 260% in 2026 even after dropping 13% on Tuesday, and has been a leader of the rebound from the S&P 500’s war-driven lows. Today's main event, the Micron earnings print, follows four of the six major market-moving events on June’s calendar: the CPI print, the SpaceX IPO, the US-Iran MoU, and Warsh’s first Fed meeting. The bar is high, positioning crowded and the semi/memory complex is nervous.

“The main problem for Micron is not Micron itself, but the expectations for its third-quarter earnings,” said Joachim Klement, head of strategy at Panmure Liberum. “Even if Micron has a stellar quarter and gives solid guidance, it may not be enough to fulfill lofty expectations.”

Traders warned of possible further swings in tech stocks if Micron’s earnings and outlook fail to meet sky-high expectations.

“For high-performing companies that reflect the dynamics of a sector, market expectations naturally rise,” said Guillermo Hernández Sampere, head of trading at MPPM. “From a rational standpoint, these are difficult to meet, and disappointments become apparent in the stock’s price performance.”

Evidence of the vast amounts of capital flowing into the buildout of AI infrastructure and its supply chain was again on display as South Korea’s SK Hynix Inc. announced it was looking to raise $29 billion in a US listing. The offering would add to the recent wave of AI-related funding secured through stock issuances, after SpaceX held the largest initial public offering in history earlier this month and Alphabet Inc. planned a $85 billion capital raise.

The sixth and final major market event on the docket this month comes on Thursday, with this week’s marquee economic release, the core PCE. Bloomberg Economics expects that a hot PCE reading will likely reinforce the hawkish tilt by the Fed at its meeting earlier this month.

Building on the AI funding theme, SK Hynix Inc. is planning to raise 45.45 trillion won ($29.4 billion) in a landmark US listing. That could put it among the top five share sales of all time, comparable with Saudi Aramco’s then-record 2019 initial public offering.

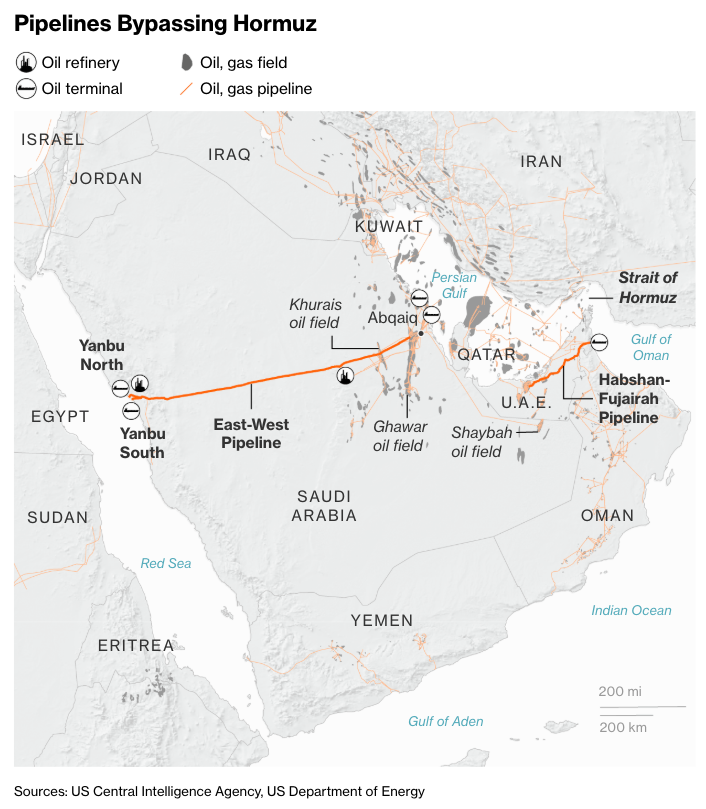

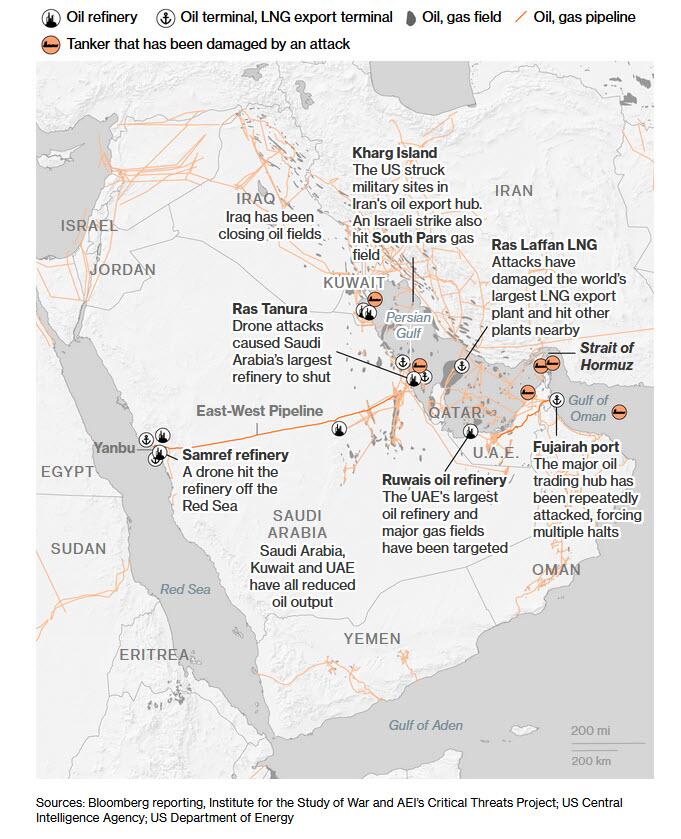

In geopolitics, oil oil is down for an eighth day in nine and back at about $72 barrel, with Brent dropping below $75 for the first time since the start of the war, as crude continues to price for lower geopolitical risk, higher supply and increasing traffic through the Strait of Hormuz. Separately, Trump is meeting defense industry executives later to talk about picking up the pace of weapon production. Lower crude prices pushed the cost of diesel in the US below $5 a gallon for the first time since mid-March.

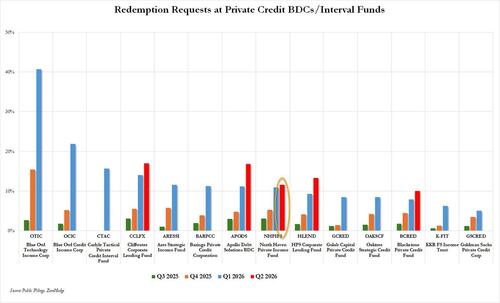

Private credit also remains in focus as a $7 billion fund run by Morgan Stanley caps investor withdrawals at 5%, allowing less than half of the redemptions shareholders requested in the second quarter.

Europe's Stoxx 600 index is little changed and Germany’s DAX is lagging following a big drop for defense company Rheinmetall. Asian stocks slid amid a selloff in the region’s leading chipmaker TSMC and other technology names over concerns about the sustainability of demand for AI-linked shares and their valuations. The MSCI Asia Pacific Index dropped as much as 1.2%, before paring most of the losses. Taiwan and Indonesia led the region’s decline, while Japan also underperformed. Indonesia’s stock benchmark fell as much as 3.7% after MSCI Inc. again decided to postpone its review on the country’s equities, saying it needs more time to see whether recently announced transparency reforms are effective. Sectors to Watch

- Chinese semiconductor stocks rally as momentum in AI‑related investments lingered, while the news about TSMC lifting prices further lifts sentiment.

- Australia’s software-heavy technology sector rises as investors rotate out of Asian chipmakers amid valuation concerns that triggered a selloff in AI-linked shares.

- India’s software exporters are steadily losing their sway on the country’s stock market as concerns over artificial intelligence-led disruption trigger a prolonged selloff in the sector.

- Chinese shipping stocks gain after more vessels transit the Strait of Hormuz with tracking signals switched on, signaling rising confidence in the vital energy chokepoint.

- Chinese healthcare stocks advance after Citi says the sector’s current valuations fail to reflect improving fundamentals and resilient order books.

- Citigroup says this year’s 6.18 campaign was the quietest in the past 16 years, which does not bode well for June retail sales data and suggests downside risks to second-quarter earnings estimates for JD and Alibaba.

In FX, the dollar continued to benefit from haven demand as risk sentiment remained fragile. Advancing 0.3%, the greenback headed for its longest winning streak in more than a month and cemented its highest level of the year. Meanwhile, the euro has fallen to the lowest since May 2025

In rates, treasuries rose modestly as inflation worries eased, with the 10-year yield falling two basis points to 4.48% supported by similar gains for European bonds during the London session, as oil prices extend their recent slide with tankers openly crossing the Strait of Hormuz. US long-end yields are about 2bp lower with shorter maturities little changed, flattening 2s10s and 5s30s spreads by almost 2bp. 10-year is about 1bp lower near 4.47%, UK counterpart by an additional 1bp. Treasury auction cycle continues with $70 billion 5-year note; Tuesday’s 2-year sale stopped through by 0.3bp. WI 5-year yield near 4.265% is ~8bp cheaper than last month’s auction, which tailed by 0.1bp. The dollar issuance slate includes three names so far. SpaceX led a $30b, four-offering calendar on Tuesday. Issuers paid about 11bp in new issue concessions on deals that were 2.9 times covered. Focal points of US session include 5-year note auction at 1pm New York time.

In commodities, WTI crude oil futures are down around 2% near session lows as the US and Iran signal progress toward ending the war, weighing on energy prices. Brent fell below $75 for the first time since the war started. Gold slipped as the stronger dollar made bullion priced in the US currency more expensive.

US economic data calendar includes 1Q current account balance (8:30am) and May new home sales (10am). Fed speaker slate includes Governor Lisa Cook at 2pm

Market Snapshot

Top Overnight News

- Qatar’s prime minister said establishing a hotline between the US and Iran is essential to prevent rogue actors impeding the reopening of the Strait of Hormuz, as he predicted that the Gulf state would resume normal liquefied natural gas production “within a few weeks”. FT

- The US Senate voted 50-48 to pass a resolution to halt the Iran war unless US President Trump gets approval from Congress. However, the White House said Congress resolutions on Iran are non-binding and won't be sent to President Trump, while Trump criticised the Senate passage of the Iran war powers resolution, which he claimed provides aid and comfort for the enemy.

- Treasury Secretary Bessent said inflation will return to the target, and he is confident Fed Chair Warsh will optimize the path for the economy. Bessent also stated that the US housing issue is a conundrum affected by rate-lock owners, and will take lower rates and more supply, predicting inflation will ease as talks with Iran continue and gas prices fall. BBG

- Congress on Tuesday passed its most-ambitious housing legislation since the 1980s, a package of more than 50 provisions aimed at making it easier to build homes and make housing more affordable. The House passed the bill 358-32 with broad bipartisan support a day after the Senate voted 85-5 to approve the measure. President Trump is expected to sign it into law as soon as Wednesday. WSJ

- Leveraged ETFs tracking Samsung Electronics or SK Hynix probably sold a combined $6 billion of the Korean chipmakers’ shares yesterday to maintain their ratios, underscoring how such products are amplifying market moves. BBG

- The BoJ sees the risk of inflation exceeding its 2% target and will conduct additional interest-rate hikes appropriately, Governor Kazuo Ueda said in speech Wednesday that reiterated policymakers’ recent messaging. BBG

- Australia’s consumer price growth eased in May amid cooling fuel prices, but underlying inflation continued to strengthen as businesses passed on higher costs resulting from the Middle East conflict. WSJ

- Extreme temperatures in Western Europe triggered widespread school and transit disruptions across the UK and France. The failure of two transformers in Brittany, probably due to the heat, left 68,000 people without electricity, while the UK’s grid operator issued a rare summer power-supply warning. BBG

- Venezuela is set to reveal a $240bn debt pile, much higher than previously thought, as the country embarks on the biggest sovereign restructuring in history following the US removal of Nicolás Maduro. The country is on track to reveal borrowings that are significantly larger than market estimates of $150bn to $200bn when it lifts the veil for creditors on the state of its finances in the coming weeks. FT

- SK Hynix plans to raise up to $29.4 billion in a landmark US listing to increase its capacity to meet memory chip demand. At that size, the deal would be among the top five share sales of all time. BBG

A more detailed look at global markets courtesy of Newsquawk

APAC stocks saw mixed price action as the initial rebound from the prior day's tech-driven sell-off gradually waned in the absence of any fresh major catalysts. ASX 200 traded rangebound as strength in tech and defensives was counterbalanced by losses in mining and energy following the recent declines in underlying commodity prices, while inflation data was mixed and would likely have little bearing on monetary policy. Nikkei 225 failed to sustain early gains and dipped back beneath the 70,000 level, while Services PPI data printed in line with forecasts and the BoJ Summary of Opinions showed members continued to advocate for further rate increases. Hang Seng and Shanghai Comp were indecisive as the attention turned to the WEF in Dalian, where Premier Li said China's economy shows resilience and maintains sound momentum. He stated China remains committed to opening up and will continue to accelerate the large-scale application of new technologies.

Top Asian News

- Japan is reportedly looking at ways to streamline the management of its USD 1.3tln FX reserves to increase returns and help state finances, Reuters reported.

- A draft proposal of 1% consumption tax was presented and will reportedly be implemented from April 2027, FNN reported. The proposal faces significant resistance from opposition parties, with DPP representative Furukawa stating they have no intention of cooperating, leaving the prospect of a June agreement uncertain.

- Chinese Premier Li said China's economy shows resilience and maintains sound momentum, while he noted four key words for the economy including stability, innovation, dynamism and integration. Li also stated that China remains committed to opening up, as well as noted that China's AI sector sees explosive growth, and they will continue to accelerate the large-scale application of new technologies.

European bourses (STOXX 600 U/C) start Wednesday's trade broadly lower, with the AEX (+0.3%) outperforming as tech names steady from Tuesday's selloff. Germany's DAX 40 (-0.9%) is the clear underperformer, as Rheinmetall weighs on the index. The FT reported that Germany will scrap plans to build Rheinmetall's F126 frigates and instead purchase 8 Meko A-200 frigates from TKMS. Rheinmetall (-14%) has taken a hit following this news, while TKMS (+9.4%) benefits. European sectors print a mixed picture. Real Estate (+2.2%) is the clear outperformer, with Food, Beverages & Tobacco (+1.1%) and Consumer Products (+1.2%) rounding out the top 3. Media (-1.3%), Construction (-0.7%) and Energy (-0.6%) are the sector laggards.

Top European News

- UK MP Jones said that while he has the 81 seats required to run, he will not contest against Burnham for Labour leadership, Sky News reported. Jones further said he thinks traders "can be content" with Burnham as PM and added that he thinks there is room to "borrow a little more", and things (referring to investment) can be done differently, without "broad brush" borrowing and spending.

- Germany confirmed earlier reports that it will abandon plans to build 6 Rheinmetall (RHM GY) F126 frigates, and instead intends to buy 8 smaller Meko A-200 frigates from TKMS (TKMS GY).

FX

- G10s are weaker against the Buck as the risk-off mood continues into Micron earnings this evening. Antipodeans lag, as the Aussie digests mixed CPI, JPY fluctuates either side of unchanged, and EMs are getting hit.

- Markets are reluctant to buy the dip in equities after losses on Tuesday. As such, the Buck continues to firm as the preferred haven, with USD outperformance vs Scandis and Antipodeans with liquidity lower. Traditional havens fare better against the Buck, JPY steady at the lower end of its recent ranges, while CHF continues its downward trend. For US-specifics, the highlight of the session will be the Fed Bank Stress Test Report alongside Micron earnings - both due after the close. DXY trades at the upper end of its 101.35-101.68 range, higher by 0.2%.

- Aussie data was mixed, CPI in May cooled below expectations, and the trimmed mean firming in line with most forecasts to 0.4% M/M and 3.6% Y/Y. The report noted housing was the main inflation pressure point, and Westpac analysis notes price pressures are broadening, particularly within services. As such, with the recent energy related prices pressures set to linger, the RBA will be keenly monitoring signs of sticky inflation with the bank widely expected to have concluded tightening. AUD faring better than Kiwi (AUD/NZD +0.1%), but lower against the Buck as the mixed data does not provide a bias towards any future easing/tightening; Labour market data ahead.

- EUR and GBP are lacklustre and tracking the firmer Buck. Domestic catalysts light for both regions, though some continued incrementally optimistic updates from a likely incoming Burnham premiership which has helped GBP. EUR/GBP trades a whisker away from the 200 week moving average @ 0.8602 which is also the session low. For the EUR, recent Governing Council commentary remains hawkish, though nothing deviating too much from the Statement at June’s meeting.

- Barclays sees a moderate dollar-buying by month-end against most majors, with a weak sign on USDJPY.

Fixed Income

- Global fixed income benchmarks are slightly firmer, as energy prices continue to pull back and investors seemingly return to see bonds as a haven following the recent tech sell-off.

- USTs (+2 ticks) return to gains after pulling back from a 109-17+ top in Tuesday's session, currently trading at the top end of a 109-09+ to 109-15 range. The US data docket is light today, ahead of Thursday's busy day (PCE, GDP, initial jobless claims, durable goods). On the supply front, the US is to sell USD 70bln 5-year notes. The auction benefits from a combination of higher outright yields, reduced geopolitical uncertainty and a more hawkish Federal Reserve. The key question will be whether the improved backdrop can bring direct bidders back into the sector while maintaining the strong indirect demand seen at the previous auction.

- Bunds (+11 ticks) have been seen as attractive in recent sessions. Analysts see value in long-end German debt, with UBS stating that yields should be capped given any further hike by the ECB is expected to be quickly reversed as it would worsen the trade-off to growth, while rates strategists at Commerzbank say Bunds remain better supported as tech stocks struggle and worries of an AI-bubble. The German IFO data was mixed, with current conditions beating estimates while expectations came in soft; however, no move resulted. German 10yr yield has now returned to 2.90%, with Bunds currently trading at the top end of its 126.67-126.98 range.

- Gilts (+18 ticks) outperform, supported by the lower energy prices and the removal of some political risk premium after Starmer's chief secretary (and former chancellor) Jones said he will not contest against Burnham for the top job. Jones also thinks the bond market can be content with Burnham as PM. Analysts at ING see limited upward risk in terms of rates, but state that political uncertainties are likely to keep upward pressure on gilts, especially the longer end. UK 10yr gilts currently in a 89.33-89.64 range.

- Germany sells EUR 1.785bln vs exp. EUR 2bln 4.00% 2037 and 3.40% 2047 Bund.

- The UK sells GBP 4.25bln 4.125% 2031 Treasury Gilt: b/c 3.47x (prev. 3.36x), average yield 4.284% (prev. 4.651%), tail 0.1bps (prev. 0.2bps).

- Italy sells EUR 2.5bln vs exp. EUR 2-2.5bln 2.20% 2028 BTP and EUR 1.75bln vs exp. EUR 1.5-1.75bln 2.40% 2039 BTPei Auctions.

Commodities

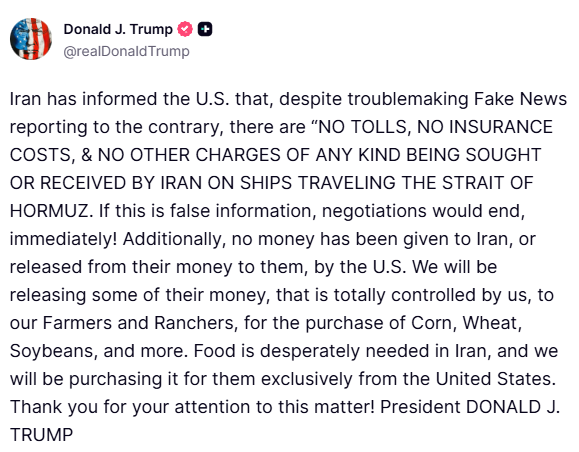

- In geopolitics, the US and Iran are continuing to finalise an agreement within the 60-day negotiation period. Amidst the talks, US President Trump reiterated that they are making a deal with Iran and will see how it goes. Currently, there are conflicting remarks made by US and Iranian officials. There appears to be disagreements surrounding the inspection of Iranian nuclear sites, and on potential tolling of the Strait of Hormuz.

- WTI and Brent are continuing to decline, posting losses of c. 2%. This comes amidst the continued flow of ships traversing through the Strait of Hormuz, albeit still remaining far below pre-war levels. From an oil perspective, estimates suggest that around 6-7mln bpd of oil went through the Strait in the past few days (vs 20mln bpd pre-war). Elsewhere, focus has also been on comments via the Russian Deputy PM Novak, who stated that the country is mulling a diesel export ban, to help ease domestic shortages. Brent Aug’26 currently trades at the bottom end of a 75.53-77.00/bbl range.

- Dutch TTF remains fairly steady, despite the Hormuz flows as focus remains on the heatwave across most of Europe. Attention has also been on French nuclear reactors, which typically need to be shut if the plant cannot cool itself efficiently. Already some EDF reactors have had to shut or taper output, but on the whole France’s national power grid operator said France has enough capacity to meet recent demand.

- Spot gold continues to extend on Tuesday’s losses, and has made a WTD trough at 4,050.47/oz (vs USD 4,115/oz peak). Action which is a continuation of recent losses, stemming from the hawkish repricing at the Fed, stronger USD/higher yields and as sell-side banks continue to trim their PT for the yellow-metal. 3M LME copper trades at the lower end of a USD 13,358-13,483.1/t range.

- US Private Inventory Data (bbls): Crude -0.8mln (exp. -5.0mln), Distillates +1.4mln (exp. -0.4mln), Gasoline +1.2mln (exp. -0.4mln), Cushing -1.0mln.

- US President Trump commented that the big oil companies are not dropping their prices at the pump commensurate with the lower prices they are paying for oil and customers are being 'gouged', while he has instructed the DoJ to look into this and stated that gasoline prices better start going down a lot faster than he is seeing.

- Qatar's PM and Foreign Minister said that the country will resume normal LNG output within weeks, according to the FT.

- Jera Chairman said that restoring Qatar’s LNG facilities, which were damaged during the Iran war, may likely take more than two or three years.

Trade/Tariffs

- Brazil will maintain its scheduled tariff hikes on imported electric and hybrid vehicles, with a 35% import tax on assembled and semi-assembled EVs taking effect in July, while disassembled vehicles will face the same rate from January 1st, 2027. Brazil will also introduce additional zero-duty import quotas for disassembled and semi-assembled EVs starting July 1st, providing limited relief for automakers amid higher import barriers.

Central Banks

- BoJ's Ueda said the timing and pace of future hikes will be decided by scrutinising the likelihood of baseline forecasts materialising, as well as risks. He added that there is risks that underlying inflation may overshoot 2%, but that Japan's economy is recovering moderately albeit with some weakness. Financial environment remains accommodative after recent rate hike; continues to support economic activity.

- BoJ Summary of Opinions from the June meeting noted a member said it has become more appropriate to adjust the degree of monetary support as FX moves are pushing up import prices, and a member said it is appropriate to continue raising interest rates as financial conditions are accommodative. There was also the opinion that even after a June rate hike, the BoJ must maintain its stance of proceeding with further rate hikes if the economy and prices move in line with forecasts. The Summary of Opinions also stated they must push up the BoJ's policy rate closer to the neutral rate as soon as possible and to near neutral at an early date to avoid big and sharp rate hikes in the future. Furthermore, a member said Japan's neutral rate is seen at around 2%, and the BoJ must raise its rates once every few months, while a member said there was no reason for the BoJ to halt a reduction in its JGB purchases.

- RBA’s Hauser said that there have been important economic developments since May and not least the chance of a US-Iran deal. Hauser said the RBA took proactive policy action to reduce excessive capacity pressures through rate hikes, while timely policy steps to reduce inflation could have lower unemployment costs. The RBA still has work to do to reduce inflation, which remains far too high.

- Riksbank Minutes (Jun): Governor Thedeen said it is reasonable to indicate that it is now somewhat more likely that we will raise the policy rate in the future. I think that this forecast is still reasonable, given the signals now coming with regard to a solution to the war between Iran and the United States.

Geopolitics: Middle East

- Pakistan's Foreign Ministry said it is conducting communications between US and Iran to effectively implement the MoU and that technical talks will continue next week; potentially Monday or Tuesday.

- Israel and Lebanon are in talks on a US-supported pilot project involving the withdrawal of Israeli troops from some parts of southern Lebanon and hand it over to Lebanese forces, according to several Israeli officials.

- Iranian Parliament Speaker Ghalibaf said Iran extends its hand of brotherhood and cooperation to all countries in the region and is ready to establish security agreements with all countries in the Middle East.

- Iranian senior commander said Iran's military has shifted to an aggressive doctrine.

- Oman established a temporary shipping lane in the Strait of Hormuz, according to IRNA. Furthermore, the Maritime Security Center in Muscat said Oman coordinates with the IMO for ships to pass through the Strait of Hormuz "without fees", according to Al Jazeera.

- Israeli Military reportedly preparing for redeployment in southern Lebanon, Al Hadath reported citing Maariv.

- Israeli tanks advanced towards Beit Yahoun in Lebanon, with heavy gunfire reported near Beit Yahoun and Kounin, while it was also reported that Israeli strikes hit the Lebanese coastal city of Tyre. Furthermore, Israeli fighter jets reportedly attacked a school in the At-Tuffah neighbourhood in eastern Gaza, and Israeli military entered Syria's Quneitra province.

Geopolitics: Ukraine

- Russia is reportedly considering a new wave of mobilisation as early as October 2026.

- Russia gas plant in Orenburg was targeted overnight by drones, Kyiv Post reported.

Geopolitics: Other

- North Korea leader Kim Jong-un said North Korea will build two Choe Hyon-class warships annually over the next five years, as it advances the nuclearisation and strategic expansion of its navy, while Kim said they will equip their destroyers with nuclear weapons.

US Event Calendar

- 7:00 am: United States Jun 19 MBA Mortgage Applications, prior -3.8%

- 8:30 am: United States 1Q Current Account Balance, est. -208.9b, prior -190.74b

- 10:00 am: United States May New Home Sales, est. 639.89k, prior 622k

- 2:00 pm: United States Fed’s Cook Gives Pre-Recorded Opening Remarks

DB's Jim Reid concludes the overnight wrap

After chipmakers led a continued US tech sell-off last night, the market mood is more mixed in Asia this morning. Korea’s KOSPI (+0.82%) is rebounding after yesterday’s sharp -9.99% drop, initially rising around 4% as heavyweights Samsung (+4.35% vs. -12.90% yesterday), recover, although SK Hynix (-2.96% vs -13.18% yesterday) continues to hover around its losses. Elsewhere, the Nikkei (-1.80%) is registering a steeper decline, while China is mixed with the CSI 300 (+0.12%) up and the Shanghai Composite (-0.25%) down. The Hang Seng (+0.04%) and Australia’s S&P/ASX 200 (+0.07%) remains marginally flat. And this morning, US equity futures have risen, with those on the S&P 500 (+0.17%) pointing to a modest recovery after the index fell -1.44% yesterday, while Nasdaq 100 futures are up +0.39%. 10yr USTs are also -1.2bps lower and hovering around 4.49% as we go to print.

Elsewhere this morning, the yen is hovering near its weakest since 1986 (161.55 against the US dollar) as concerns that Japanese authorities may intervene to curb further losses continues. The yen’s low follows the BoJ’s latest summary of opinions that came out earlier overnight, where policy members continued to press for further rate hikes after the group raised Japan’s policy rate to 1% last week, although the summary did not mention when the likely timing of the next move will be. As a reminder, our Japan economist forecasts the next BoJ hike to be this October, followed by quarterly hikes thereafter until reaching 1.75% in April 2027. 10yr JGBs (+0.4bbps) are slightly higher as I type.

We also had overnight data that showed Australia’s CPI rose +4.0% y/y in May (vs +4.3% est and +4.2% prior). Trimmed mean CPI edged up to +3.6% y/y from +3.4% prior. So while the softer headline suggests easing inflation—helped by lower oil prices amid easing US–Iran tensions—underlying pressures remain sticky, likely keeping the RBA on a hawkish footing.

Ahead of those overnight developments, markets saw a classic risk-off move yesterday, with equities sliding and bonds rallying. The main catalyst was another selloff in tech stocks, and chips in particular. Indeed, the Philly semiconductor index (-7.87%) saw its biggest fall since the jobs report at the start of the month, back when it fell over -10% in a single day. This decline included Sandisk (-13.64%) and Micron (-13.18%) as the two worst performers in the S&P 500 yesterday, though they remain among top four performers YTD. Given the importance of semiconductors for US equities, that dragged down the broader indices, with the NASDAQ slumping -2.21% yesterday, whilst the S&P 500 fell -1.44%. Indeed, the concentration of the decline was striking, as it was the first time this year that the S&P 500 was down more than 1% on a day when majority of companies in the index were actually higher. Over in Europe, the divergence wasn’t quite so marked, but the STOXX 600 (-0.73%) still posted its worst day in three weeks as tech stocks led the declines.

Interestingly, this equity weakness happened despite a couple of good news stories on the economy yesterday. The first was the flash PMIs for June, which generally surprised on the upside, suggesting that the global economy was still coping better with the energy shock than many expected. Indeed, the US composite PMI hit a 5-month high of 52.2 (vs. 51.1 expected), a level we haven’t seen since the Iran conflict began. And in the Euro Area, the composite PMI also rose more than expected to 49.5 (vs. 49.2 expected), so collectively the numbers painted a decent narrative about the global economy at the end of Q2.

On top of the PMIs, yesterday also saw a fresh tailwind in the form of lower energy prices, with Brent crude (-1.05%) down to a 3-month low of $77.08/bbl. That came as investors remained hopeful that the shipping through the Strait of Hormuz would normalise before long, with data pointing to more vessels going through, even if they’re only creeping up slowly. On the topic of the Strait of Hormuz, we also have a DBRI note (link here) looking at the path to normalisation, the implications, and an analysis of the different sectors impacted by the closure. It's a collaboration between numerous macro and micro analysis and is a comprehensive look at where various products and sector are after several weeks of the strait being closed and now reopening.

With oil prices coming down, that helped to ease fears about stagflation considerably. In fact, the US 1yr inflation swap (-7.1bps) fell to just 2.28%, which is actually beneath its level before the Iran conflict began. And similarly, the Euro 1yr inflation swap (-8.0bps) fell to 2.45%, its lowest since early March. So that led investors to price out the chance of rapid rate hikes this year, with futures pricing 38bps of Fed rate hikes by December, down -3.0bps from its cycle high the previous day. And for the ECB it was much the same story, with just 31bps of cuts priced by December, down -1.1bps on the day.

That backdrop of lower oil prices, easing inflation fears, and more dovish rates pricing was very supportive for sovereign bonds. In fact, the 10yr bund yield (-3.2bps) hit a 3-month low of 2.92%, whilst yields on 10yr OATs (-2.8bps) and BTPs (-1.0bps) also fell. That came in spite of comments from ECB chief economist Lane, who said that ECB officials faced the risk of inflation remaining above target “for quite some time”. But ultimately, the deflationary impact of lower oil prices helped to ease fears about a more hawkish response yesterday. Indeed, US Treasuries saw a similar impact, with the 10yr yield (-1.2bps) slipping back to 4.50%.

One exception from the largely positive data picture was Germany, whose flash composite PMI fell to 48 from 48.8 in May, notably below the 49.7 expected with services being the main drag. However, the survey was before the MoU was signed between the US and Iran so analysts will be looking for a recovery in the final figures. Staying with Germany, Marion Muehlberger highlights a positive surprise in the pension reform plans announced yesterday. Her piece (link here) discusses the introduction of a mandatory funded component, with an additional 2pp of gross salaries to be invested in a centralised public pension fund, phased in gradually until 2031. This is expected to result in around €35bn of additional investment into capital markets, with no pre-defined asset allocation or country split. Sweden’s “premium pension” serves as a model. As well as improving the sustainability of Germany’s public pension system in the context of an ageing population, this could also provide a meaningful boost to German and European capital markets.

Here in the UK, gilts outperformed yesterday after the flash PMIs were also weaker than expected. The composite PMI unexpectedly fell to 49.4 (vs. 50.5 expected), meaning it was still in contractionary territory. So coupled with the decline in oil prices, that led to growing doubt about a Bank of England rate hike happening this year. In turn, that meant the 10yr gilt yield fell -5.4bps to 4.75%, a bigger decline than the other big European economies. Meanwhile on the political scene, Andy Burnham is still the only declared candidate at present to become the next Labour leader and PM. So if that stays the case (and any candidate still needs 20% of Labour MPs to nominate them), Burnham could theoretically become the new leader as soon as mid-July.

Looking at the day ahead, and data releases include the Ifo’s business climate indicator from Germany, and US new home sales for May. From central banks, we’ll hear from the ECB’s Nagel, Cipollone and Moulin, along with the BoE’s Breeden and Dhingra. Finally, today’s earnings include Micron.

Tyler Durden

Wed, 06/24/2026 - 08:25

Democratic congressional candidate Brad Lander (R) arrives with New York City Mayor Zohran Mamdani for an election night watch party in New York City on June 23, 2026. Ryan Murphy/AP Photo

Democratic congressional candidate Brad Lander (R) arrives with New York City Mayor Zohran Mamdani for an election night watch party in New York City on June 23, 2026. Ryan Murphy/AP Photo Shaughna Bishop and her son Cole Bishop said the debate over regulating artificial intelligence affected their decision. They voted in Manhattan, N.Y., on June 23, 2026. Nick Zifkac/The Epoch Times

Shaughna Bishop and her son Cole Bishop said the debate over regulating artificial intelligence affected their decision. They voted in Manhattan, N.Y., on June 23, 2026. Nick Zifkac/The Epoch Times

Image: Prime Minister of Armenia's Press Service

Image: Prime Minister of Armenia's Press Service

A person votes in the Virginia redistricting referendum at Lyles-Crouch Traditional Academy, Tuesday, April 21, 2026, in Alexandria, Va. AP Photo/Julia Demaree Nikhinson

A person votes in the Virginia redistricting referendum at Lyles-Crouch Traditional Academy, Tuesday, April 21, 2026, in Alexandria, Va. AP Photo/Julia Demaree Nikhinson

Recent comments